Having covered the basics of continuous-time processes and filtrations in the previous posts, I now move on to stochastic integration. In standard calculus and ordinary differential equations, a central object of study is the derivative

However, the kinds of processes studied in stochastic calculus are much less well behaved. For example, with probability one, the sample paths of standard Brownian motion are nowhere differentiable. Furthermore, they have infinite variation over bounded time intervals. Consequently, if

Stochastic integration with respect to standard Brownian motion was developed by Kiyoshi Ito. This required restricting the class of possible integrands to be adapted processes, and the integral can then be constructed using the Ito isometry. This method was later extended to more general square integrable martingales and, then, to the class of semimartingales. It can then be shown that, as with Lebesgue integration, a version of the bounded and dominated convergence theorems are satisfied.

In these notes, a more direct approach is taken. The idea is that we simply define the stochastic integral such that the required elementary properties are satisfied. That is, it should agree with the explicit expressions for certain simple integrands, and should satisfy the bounded and dominated convergence theorems. Much of the theory of stochastic calculus follows directly from these properties, and detailed constructions of the integral are not required for many practical applications. Continue reading “The Stochastic Integral”

of stopping times increasing to infinity such that the stopped processes

of stopping times increasing to infinity such that the stopped processes  are martingales. Local submartingales and local supermartingales are defined similarly.

are martingales. Local submartingales and local supermartingales are defined similarly. representing his net gain (or loss) just before the n’th toss. Let

representing his net gain (or loss) just before the n’th toss. Let  be a sequence of independent random variables with

be a sequence of independent random variables with  . Here,

. Here,  represents the outcome of the n’th toss, with 1 referring to a head and -1 referring to a tail. Set

represents the outcome of the n’th toss, with 1 referring to a head and -1 referring to a tail. Set  and

and

. Letting

. Letting  then the optional stopping theorem shows that

then the optional stopping theorem shows that  is a uniformly bounded martingale on

is a uniformly bounded martingale on  , continuous at

, continuous at  , and constant on

, and constant on  . This is therefore a martingale, showing that

. This is therefore a martingale, showing that ![{{\mathbb E}[X_1]=1\not={\mathbb E}[X_0]=0}](https://s0.wp.com/latex.php?latex=%7B%7B%5Cmathbb+E%7D%5BX_1%5D%3D1%5Cnot%3D%7B%5Cmathbb+E%7D%5BX_0%5D%3D0%7D&bg=ffffff&fg=000000&s=0&c=20201002) , so it is not a martingale.

, so it is not a martingale.  such that the stopped processes

such that the stopped processes

for the processes locally in P. Choosing the sequence

for the processes locally in P. Choosing the sequence  of stopping times shows that

of stopping times shows that  . A class of processes is said to be stable if

. A class of processes is said to be stable if  is in P whenever X is, for all stopping times

is in P whenever X is, for all stopping times  . For example, the

. For example, the  is uniformly integrable. However, even if this is the case, it does not follow that the set of values of the process sampled at arbitrary stopping times is uniformly integrable.

is uniformly integrable. However, even if this is the case, it does not follow that the set of values of the process sampled at arbitrary stopping times is uniformly integrable. is any fixed time then this says that

is any fixed time then this says that ![{X_\tau={\mathbb E}[X_t\mid\mathcal{F}_\tau]}](https://s0.wp.com/latex.php?latex=%7BX_%5Ctau%3D%7B%5Cmathbb+E%7D%5BX_t%5Cmid%5Cmathcal%7BF%7D_%5Ctau%5D%7D&bg=ffffff&fg=000000&s=0&c=20201002) for stopping times

for stopping times  . As sets of conditional expectations of a random variable are uniformly integrable, the following result holds.

. As sets of conditional expectations of a random variable are uniformly integrable, the following result holds.

is uniformly integrable.

is uniformly integrable. is uniformly integrable.

is uniformly integrable. converges uniformly on compacts to a limit

converges uniformly on compacts to a limit ![{[0,t]}](https://s0.wp.com/latex.php?latex=%7B%5B0%2Ct%5D%7D&bg=ffffff&fg=000000&s=0&c=20201002) . That is,

. That is,

.

. converges to the limit

converges to the limit

.

.  . The absolute maximum process of a martingale is denoted by

. The absolute maximum process of a martingale is denoted by  . For any real number

. For any real number  , the

, the  -norm of a random variable

-norm of a random variable  is

is![\displaystyle \Vert Z\Vert_p\equiv{\mathbb E}[|Z|^p]^{1/p}.](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%5CVert+Z%5CVert_p%5Cequiv%7B%5Cmathbb+E%7D%5B%7CZ%7C%5Ep%5D%5E%7B1%2Fp%7D.+&bg=ffffff&fg=000000&s=0&c=20201002)

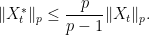

-norm of its terminal value, and bound the

-norm of its terminal value, and bound the  .

. . Then

. Then  ,

,

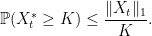

![\displaystyle \lVert X^*_t\rVert_1\le\frac e{e-1}{\mathbb E}\left[\lvert X_t\rvert \log\lvert X_t\rvert+1\right].](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%5ClVert+X%5E%2A_t%5CrVert_1%5Cle%5Cfrac+e%7Be-1%7D%7B%5Cmathbb+E%7D%5Cleft%5B%5Clvert+X_t%5Crvert+%5Clog%5Clvert+X_t%5Crvert%2B1%5Cright%5D.+&bg=ffffff&fg=000000&s=0&c=20201002)

is bounded above by some finite value as

is bounded above by some finite value as  runs through the positive reals.

runs through the positive reals. exists and is finite, with probability one.

exists and is finite, with probability one.  , the argument is a relatively basic application of elementary integrals. For simple stopping times

, the argument is a relatively basic application of elementary integrals. For simple stopping times  , the stochastic interval

, the stochastic interval ![{(\sigma,\tau]}](https://s0.wp.com/latex.php?latex=%7B%28%5Csigma%2C%5Ctau%5D%7D&bg=ffffff&fg=000000&s=0&c=20201002) and its indicator function

and its indicator function ![{1_{(\sigma,\tau]}}](https://s0.wp.com/latex.php?latex=%7B1_%7B%28%5Csigma%2C%5Ctau%5D%7D%7D&bg=ffffff&fg=000000&s=0&c=20201002) are elementary predictable. For any submartingale

are elementary predictable. For any submartingale ![\displaystyle {\mathbb E}\left[X_\tau-X_\sigma\right]={\mathbb E}\left[\int_0^\infty 1_{(\sigma,\tau]}\,dX\right]\ge 0.](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%7B%5Cmathbb+E%7D%5Cleft%5BX_%5Ctau-X_%5Csigma%5Cright%5D%3D%7B%5Cmathbb+E%7D%5Cleft%5B%5Cint_0%5E%5Cinfty+1_%7B%28%5Csigma%2C%5Ctau%5D%7D%5C%2CdX%5Cright%5D%5Cge+0.+&bg=ffffff&fg=000000&s=0&c=20201002)

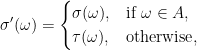

the following

the following

by

by  extends inequality (

extends inequality (![\displaystyle {\mathbb E}\left[1_A(X_\tau-X_\sigma)\right]={\mathbb E}\left[X_\tau-X_{\sigma^\prime}\right]\ge 0.](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%7B%5Cmathbb+E%7D%5Cleft%5B1_A%28X_%5Ctau-X_%5Csigma%29%5Cright%5D%3D%7B%5Cmathbb+E%7D%5Cleft%5BX_%5Ctau-X_%7B%5Csigma%5E%5Cprime%7D%5Cright%5D%5Cge+0.+&bg=ffffff&fg=000000&s=0&c=20201002)

it implies the extension of the submartingale property

it implies the extension of the submartingale property ![{X_\sigma\le{\mathbb E}[X_\tau\vert\mathcal{F}_\sigma]}](https://s0.wp.com/latex.php?latex=%7BX_%5Csigma%5Cle%7B%5Cmathbb+E%7D%5BX_%5Ctau%5Cvert%5Cmathcal%7BF%7D_%5Csigma%5D%7D&bg=ffffff&fg=000000&s=0&c=20201002) to the random times. This argument applies to all simple stopping times, and is sufficient to prove the optional sampling result for discrete time submartingales. In continuous time, the additional hypothesis that the process is right-continuous is required. Then, the result follows by taking limits of simple stopping times.

to the random times. This argument applies to all simple stopping times, and is sufficient to prove the optional sampling result for discrete time submartingales. In continuous time, the additional hypothesis that the process is right-continuous is required. Then, the result follows by taking limits of simple stopping times. are integrable and the following are satisfied.

are integrable and the following are satisfied. ![{X_\sigma={\mathbb E}\left[X_{\tau}\vert\mathcal{F}_\sigma\right].}](https://s0.wp.com/latex.php?latex=%7BX_%5Csigma%3D%7B%5Cmathbb+E%7D%5Cleft%5BX_%7B%5Ctau%7D%5Cvert%5Cmathcal%7BF%7D_%5Csigma%5Cright%5D.%7D&bg=ffffff&fg=000000&s=0&c=20201002)

![{X_\sigma\le{\mathbb E}\left[X_{\tau}\vert\mathcal{F}_\sigma\right].}](https://s0.wp.com/latex.php?latex=%7BX_%5Csigma%5Cle%7B%5Cmathbb+E%7D%5Cleft%5BX_%7B%5Ctau%7D%5Cvert%5Cmathcal%7BF%7D_%5Csigma%5Cright%5D.%7D&bg=ffffff&fg=000000&s=0&c=20201002)

![{X_\sigma\ge{\mathbb E}\left[X_{\tau}\vert\mathcal{F}_\sigma\right].}](https://s0.wp.com/latex.php?latex=%7BX_%5Csigma%5Cge%7B%5Cmathbb+E%7D%5Cleft%5BX_%7B%5Ctau%7D%5Cvert%5Cmathcal%7BF%7D_%5Csigma%5Cright%5D.%7D&bg=ffffff&fg=000000&s=0&c=20201002)

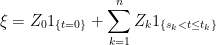

(and

(and  ). The jump at time

). The jump at time  .

.

,

,  -measurable random variable

-measurable random variable  and

and  -measurable random variables

-measurable random variables  . Its integral with respect to a stochastic process

. Its integral with respect to a stochastic process

which is a finite union of sets of the form

which is a finite union of sets of the form  for

for  and

and ![{(s,t]\times F}](https://s0.wp.com/latex.php?latex=%7B%28s%2Ct%5D%5Ctimes+F%7D&bg=ffffff&fg=000000&s=0&c=20201002) for nonnegative reals

for nonnegative reals  and

and  . Then, a process is an indicator function

. Then, a process is an indicator function  of some elementary predictable set

of some elementary predictable set  if and only if it is elementary predictable and takes values in

if and only if it is elementary predictable and takes values in  .

. ,

,

![\displaystyle \left\{{\mathbb E}\left[\int_0^t1_A\,dX\right]\colon A\textrm{ is elementary}\right\}](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%5Cleft%5C%7B%7B%5Cmathbb+E%7D%5Cleft%5B%5Cint_0%5Et1_A%5C%2CdX%5Cright%5D%5Ccolon+A%5Ctextrm%7B+is+elementary%7D%5Cright%5C%7D+&bg=ffffff&fg=000000&s=0&c=20201002)

whose time index

whose time index  . For real numbers

. For real numbers  , the number of upcrossings of

, the number of upcrossings of ![{[a,b]}](https://s0.wp.com/latex.php?latex=%7B%5Ba%2Cb%5D%7D&bg=ffffff&fg=000000&s=0&c=20201002) is the supremum of the nonnegative integers

is the supremum of the nonnegative integers  such that there exists times

such that there exists times  satisfying

satisfying

. The number of upcrossings is denoted by

. The number of upcrossings is denoted by ![{U[a,b]}](https://s0.wp.com/latex.php?latex=%7BU%5Ba%2Cb%5D%7D&bg=ffffff&fg=000000&s=0&c=20201002) , which is either a nonnegative integer or is infinite. Similarly, the number of downcrossings, denoted by

, which is either a nonnegative integer or is infinite. Similarly, the number of downcrossings, denoted by ![{D[a,b]}](https://s0.wp.com/latex.php?latex=%7BD%5Ba%2Cb%5D%7D&bg=ffffff&fg=000000&s=0&c=20201002) , is the supremum of the nonnegative integers

, is the supremum of the nonnegative integers  .

. converges to a limit in the extended real numbers if and only if the number of upcrossings

converges to a limit in the extended real numbers if and only if the number of upcrossings