Martingale inequalities are an important subject in the study of stochastic processes. The subject of this post is Doob’s inequalities which bound the distribution of the maximum value of a martingale in terms of its terminal distribution, and is a consequence of the optional sampling theorem. We work with respect to a filtered probability space

![\displaystyle \Vert Z\Vert_p\equiv{\mathbb E}[|Z|^p]^{1/p}.](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%5CVert+Z%5CVert_p%5Cequiv%7B%5Cmathbb+E%7D%5B%7CZ%7C%5Ep%5D%5E%7B1%2Fp%7D.+&bg=ffffff&fg=000000&s=0&c=20201002)

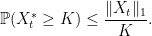

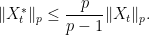

Then, Doob’s inequalities bound the distribution of the maximum of a martingale by the

Theorem 1 Let

be a cadlag martingale and

. Then

- for every

,

- for every

![\displaystyle \lVert X^*_t\rVert_1\le\frac e{e-1}{\mathbb E}\left[\lvert X_t\rvert \log\lvert X_t\rvert+1\right].](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%5ClVert+X%5E%2A_t%5CrVert_1%5Cle%5Cfrac+e%7Be-1%7D%7B%5Cmathbb+E%7D%5Cleft%5B%5Clvert+X_t%5Crvert+%5Clog%5Clvert+X_t%5Crvert%2B1%5Cright%5D.+&bg=ffffff&fg=000000&s=0&c=20201002)

We can define a topology on the space of cadlag martingales so that a sequence

The second statement above does not extend to

Doob’s martingale inequalities are a consequence of the following inequalities applied to the submartingale

Theorem 2 Let

for each

for each

.

I briefly note that the third inequality looks a bit odd, as it is not dimensionally consistent. This means that, unlike the other two, applying it to

![\displaystyle \lVert X^*_t\rVert_1\le(e/(e-1)){\mathbb E}[X_t\log X_t+c]](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%5ClVert+X%5E%2A_t%5CrVert_1%5Cle%28e%2F%28e-1%29%29%7B%5Cmathbb+E%7D%5BX_t%5Clog+X_t%2Bc%5D+&bg=ffffff&fg=000000&s=0&c=20201002)

where c is equal to ![{{\mathbb E}[X_t]\log a+1/a}](https://s0.wp.com/latex.php?latex=%7B%7B%5Cmathbb+E%7D%5BX_t%5D%5Clog+a%2B1%2Fa%7D&bg=ffffff&fg=000000&s=0&c=20201002)

![{a=1/{\mathbb E}[X_t]}](https://s0.wp.com/latex.php?latex=%7Ba%3D1%2F%7B%5Cmathbb+E%7D%5BX_t%5D%7D&bg=ffffff&fg=000000&s=0&c=20201002)

![\displaystyle \lVert X^*_t\rVert_1\le(e/(e-1))\left({\mathbb E}[X_t\log X_t]+{\mathbb E}[X_t](1-\log{\mathbb E}[X_t])\right).](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%5ClVert+X%5E%2A_t%5CrVert_1%5Cle%28e%2F%28e-1%29%29%5Cleft%28%7B%5Cmathbb+E%7D%5BX_t%5Clog+X_t%5D%2B%7B%5Cmathbb+E%7D%5BX_t%5D%281-%5Clog%7B%5Cmathbb+E%7D%5BX_t%5D%29%5Cright%29.+&bg=ffffff&fg=000000&s=0&c=20201002)

This is dimensionally consistent — replacing X by

![{{\mathbb E}[X_t\log X_t]}](https://s0.wp.com/latex.php?latex=%7B%7B%5Cmathbb+E%7D%5BX_t%5Clog+X_t%5D%7D&bg=ffffff&fg=000000&s=0&c=20201002)

To prove Theorem 2, we start with the following submartingale inequality from which each of Doob’s inequalities will follow.

Lemma 3 Let

,

(1)

![\displaystyle K{\mathbb P}(X^*_t\ge K)\le{\mathbb E}\left[1_{\{X^*_t\ge K\}}X_t\right].](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++K%7B%5Cmathbb+P%7D%28X%5E%2A_t%5Cge+K%29%5Cle%7B%5Cmathbb+E%7D%5Cleft%5B1_%7B%5C%7BX%5E%2A_t%5Cge+K%5C%7D%7DX_t%5Cright%5D.+&bg=ffffff&fg=000000&s=0&c=20201002)

Proof: By completing the filtration if necessary, without loss of generality we assume that it is complete. Consider the first time at which the process reaches a positive value

which, by the debut theorem, is a stopping time. Then

![\displaystyle L1_{\{X^*_t \ge K\}}\le 1_{\{\tau\le t\}}X_\tau \le {\mathbb E}[1_{\{X^*_t\ge L\}}X_t\vert\mathcal{F}_\tau].](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++L1_%7B%5C%7BX%5E%2A_t+%5Cge+K%5C%7D%7D%5Cle+1_%7B%5C%7B%5Ctau%5Cle+t%5C%7D%7DX_%5Ctau+%5Cle+%7B%5Cmathbb+E%7D%5B1_%7B%5C%7BX%5E%2A_t%5Cge+L%5C%7D%7DX_t%5Cvert%5Cmathcal%7BF%7D_%5Ctau%5D.+&bg=ffffff&fg=000000&s=0&c=20201002)

Taking expectations

![\displaystyle L{\mathbb P}(X^*_t\ge K)\le {\mathbb E}[1_{\{X^*_t\ge L\}}X_t],](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++L%7B%5Cmathbb+P%7D%28X%5E%2A_t%5Cge+K%29%5Cle+%7B%5Cmathbb+E%7D%5B1_%7B%5C%7BX%5E%2A_t%5Cge+L%5C%7D%7DX_t%5D%2C+&bg=ffffff&fg=000000&s=0&c=20201002)

and (1) follows by letting L increase to K. ⬜

We use (1) to prove Doob’s inequalities.

Proof of Theorem 2: Bounding the right hand side of (1) by ![{{\mathbb E}[X_t]}](https://s0.wp.com/latex.php?latex=%7B%7B%5Cmathbb+E%7D%5BX_t%5D%7D&bg=ffffff&fg=000000&s=0&c=20201002)

![\displaystyle \setlength\arraycolsep{2pt} \begin{array}{rcl} \displaystyle{\mathbb E}\left[(L\wedge X^*_t)^p\right] &\displaystyle=&\displaystyle p{\mathbb E}\left[\int_0^L K^{p-1} 1_{\{X^*_t\ge K\}}\,dK\right]\smallskip\\ &\displaystyle=&\displaystyle p\int_0^L K^{p-1}{\mathbb P}(X^*_t\ge K)\,dK\smallskip\\ &\displaystyle\le &\displaystyle p\int_0^L K^{p-2}{\mathbb E}\left[1_{\{X^*_t\ge K\}}X_t\right]\,dK\smallskip\\ &\displaystyle=&\displaystyle p{\mathbb E}\left[X_t\int_0^{L\wedge X^*_t}K^{p-2}\,dK\right]\smallskip\\ &\displaystyle=&\displaystyle\frac{p}{p-1}{\mathbb E}\left[X_t(L\wedge X^*_t)^{p-1}\right]. \end{array}](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%5Csetlength%5Carraycolsep%7B2pt%7D+%5Cbegin%7Barray%7D%7Brcl%7D+%5Cdisplaystyle%7B%5Cmathbb+E%7D%5Cleft%5B%28L%5Cwedge+X%5E%2A_t%29%5Ep%5Cright%5D+%26%5Cdisplaystyle%3D%26%5Cdisplaystyle+p%7B%5Cmathbb+E%7D%5Cleft%5B%5Cint_0%5EL+K%5E%7Bp-1%7D+1_%7B%5C%7BX%5E%2A_t%5Cge+K%5C%7D%7D%5C%2CdK%5Cright%5D%5Csmallskip%5C%5C+%26%5Cdisplaystyle%3D%26%5Cdisplaystyle+p%5Cint_0%5EL+K%5E%7Bp-1%7D%7B%5Cmathbb+P%7D%28X%5E%2A_t%5Cge+K%29%5C%2CdK%5Csmallskip%5C%5C+%26%5Cdisplaystyle%5Cle+%26%5Cdisplaystyle+p%5Cint_0%5EL+K%5E%7Bp-2%7D%7B%5Cmathbb+E%7D%5Cleft%5B1_%7B%5C%7BX%5E%2A_t%5Cge+K%5C%7D%7DX_t%5Cright%5D%5C%2CdK%5Csmallskip%5C%5C+%26%5Cdisplaystyle%3D%26%5Cdisplaystyle+p%7B%5Cmathbb+E%7D%5Cleft%5BX_t%5Cint_0%5E%7BL%5Cwedge+X%5E%2A_t%7DK%5E%7Bp-2%7D%5C%2CdK%5Cright%5D%5Csmallskip%5C%5C+%26%5Cdisplaystyle%3D%26%5Cdisplaystyle%5Cfrac%7Bp%7D%7Bp-1%7D%7B%5Cmathbb+E%7D%5Cleft%5BX_t%28L%5Cwedge+X%5E%2A_t%29%5E%7Bp-1%7D%5Cright%5D.+%5Cend%7Barray%7D+&bg=ffffff&fg=000000&s=0&c=20201002)

Setting

![\displaystyle E[X_t(L\wedge X^*_t)^{p-1}]\le\Vert X_t\Vert_p\Vert(L\wedge X^*_t)^{p-1}\Vert_q = \Vert X_t\Vert_p\Vert L\wedge X^*_t\Vert_p^{p-1}.](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++E%5BX_t%28L%5Cwedge+X%5E%2A_t%29%5E%7Bp-1%7D%5D%5Cle%5CVert+X_t%5CVert_p%5CVert%28L%5Cwedge+X%5E%2A_t%29%5E%7Bp-1%7D%5CVert_q+%3D+%5CVert+X_t%5CVert_p%5CVert+L%5Cwedge+X%5E%2A_t%5CVert_p%5E%7Bp-1%7D.+&bg=ffffff&fg=000000&s=0&c=20201002)

Substituting into the previous inequality,

Finally, cancel

Now, multiply both sides of (1) by

![{[1,L]}](https://s0.wp.com/latex.php?latex=%7B%5B1%2CL%5D%7D&bg=ffffff&fg=000000&s=0&c=20201002)

![\displaystyle \setlength\arraycolsep{2pt} \begin{array}{rcl} \displaystyle{\mathbb E}\left[(L\wedge X^*_t-1)_+\right] &\displaystyle=&\displaystyle {\mathbb E}\left[\int_1^L1_{\{X^*_t\ge K\}}\,dK\right]\smallskip\\ &\displaystyle=&\displaystyle \int_1^L{\mathbb P}(X^*_t\ge K)\,dK\smallskip\\ &\displaystyle\le &\displaystyle \int_1^LK^{-1}{\mathbb E}\left[1_{\{X^*_t\ge K\}}X_t\right]\,dK\smallskip\\ &\displaystyle=&\displaystyle {\mathbb E}\left[X_t\int_1^{1\vee(L\wedge X^*_t)}K^{-1}\,dK\right]\smallskip\\ &\displaystyle=&\displaystyle{\mathbb E}\left[X_t\log_+(L\wedge X^*_t)\right], \end{array}](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%5Csetlength%5Carraycolsep%7B2pt%7D+%5Cbegin%7Barray%7D%7Brcl%7D+%5Cdisplaystyle%7B%5Cmathbb+E%7D%5Cleft%5B%28L%5Cwedge+X%5E%2A_t-1%29_%2B%5Cright%5D+%26%5Cdisplaystyle%3D%26%5Cdisplaystyle+%7B%5Cmathbb+E%7D%5Cleft%5B%5Cint_1%5EL1_%7B%5C%7BX%5E%2A_t%5Cge+K%5C%7D%7D%5C%2CdK%5Cright%5D%5Csmallskip%5C%5C+%26%5Cdisplaystyle%3D%26%5Cdisplaystyle+%5Cint_1%5EL%7B%5Cmathbb+P%7D%28X%5E%2A_t%5Cge+K%29%5C%2CdK%5Csmallskip%5C%5C+%26%5Cdisplaystyle%5Cle+%26%5Cdisplaystyle+%5Cint_1%5ELK%5E%7B-1%7D%7B%5Cmathbb+E%7D%5Cleft%5B1_%7B%5C%7BX%5E%2A_t%5Cge+K%5C%7D%7DX_t%5Cright%5D%5C%2CdK%5Csmallskip%5C%5C+%26%5Cdisplaystyle%3D%26%5Cdisplaystyle+%7B%5Cmathbb+E%7D%5Cleft%5BX_t%5Cint_1%5E%7B1%5Cvee%28L%5Cwedge+X%5E%2A_t%29%7DK%5E%7B-1%7D%5C%2CdK%5Cright%5D%5Csmallskip%5C%5C+%26%5Cdisplaystyle%3D%26%5Cdisplaystyle%7B%5Cmathbb+E%7D%5Cleft%5BX_t%5Clog_%2B%28L%5Cwedge+X%5E%2A_t%29%5Cright%5D%2C+%5Cend%7Barray%7D+&bg=ffffff&fg=000000&s=0&c=20201002)

using the notation

|

(2) |

holds for nonnegative x and y. Adding ![{{\mathbb E}[1\wedge X^*_t]}](https://s0.wp.com/latex.php?latex=%7B%7B%5Cmathbb+E%7D%5B1%5Cwedge+X%5E%2A_t%5D%7D&bg=ffffff&fg=000000&s=0&c=20201002)

![\displaystyle {\mathbb E}[L\wedge X^*_t]\le{\mathbb E}[X_t\log X_t+e^{-1}(L\wedge X^*_t)+1].](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%7B%5Cmathbb+E%7D%5BL%5Cwedge+X%5E%2A_t%5D%5Cle%7B%5Cmathbb+E%7D%5BX_t%5Clog+X_t%2Be%5E%7B-1%7D%28L%5Cwedge+X%5E%2A_t%29%2B1%5D.+&bg=ffffff&fg=000000&s=0&c=20201002)

Subtract ![{e^{-1}{\mathbb E}[L\wedge X^*_t]}](https://s0.wp.com/latex.php?latex=%7Be%5E%7B-1%7D%7B%5Cmathbb+E%7D%5BL%5Cwedge+X%5E%2A_t%5D%7D&bg=ffffff&fg=000000&s=0&c=20201002)

It only remains to show that (2) holds for all nonnegative reals x and y. Moving all the terms to the same side, the inequality is equivalent to

By differentiating with respect to x, the minimum of the left hand side occurs at

This article was really helpful, thx.

PS: in the last line the constant p/(p-1) is missing…

Fixed. Thanks.

Hi George,

Just a small comment:

I think one needs to first consider a finite time grid to be able to assume that {X_t^* >= K} = {\tau <= t} (second line in proof of theorem 2) and the use MCT to get the result for countable time and continuous time in the cadlag case, like you mentioned in the planetmath proof.

Best,

Tigran

Hi. You can do it that way, but it is not necessary to start by restricting to the finite case. I already proved the Debut theorem and optional sampling for continuous-time cadlag processes. As we assume the process is cadlag, these can be applied directly to the continuous time case.