Here, I apply the theory outlined in the previous post to fully describe the drawdown point process of a standard Brownian motion. In fact, as I will show, the drawdowns can all be constructed from independent copies of a single ‘Brownian excursion’ stochastic process. Recall that we start with a continuous stochastic process X, assumed here to be Brownian motion, and define its running maximum as and drawdown process . This is as in figure 1 above.

Next, was defined to be the drawdown ‘excursion’ over the interval at which the maximum process is equal to the value . Precisely, if we let be the first time at which X hits level and be its right limit then,

Next, a random set S is defined as the collection of all nonzero drawdown excursions indexed the running maximum,

The set of drawdown excursions corresponding to the sample path from figure 1 are shown in figure 2 below.

Figure 2: Brownian drawdown excursions

As described in the post on semimartingale local times, the joint distribution of the drawdown and running maximum , of a Brownian motion, is identical to the distribution of its absolute value and local time at zero, . Hence, the point process consisting of the drawdown excursions indexed by the running maximum, and the absolute value of the excursions from zero indexed by the local time, both have the same distribution. So, the theory described in this post applies equally to the excursions away from zero of a Brownian motion.

Before going further, let’s recap some of the technical details. The excursions lie in the space E of continuous paths , on which we define a canonical process Z by sampling the path at each time t, . This space is given the topology of uniform convergence over finite time intervals (compact open topology), which makes it into a Polish space, and whose Borel sigma-algebra is equal to the sigma-algebra generated by . As shown in the previous post, the counting measure is a random point process on . In fact, it is a Poisson point process, so its distribution is fully determined by its intensity measure .

Theorem 1 If X is a standard Brownian motion, then the drawdown point process is Poisson with intensity measure where,

is the standard Lebesgue measure on .

is a sigma-finite measure on E given by

(1)

for all bounded continuous continuous maps which vanish on paths of length less than L (some ). The limit is taken over , denotes expectation under the measure with respect to which Z is a Brownian motion started at , and is the first time at which Z hits 0. This measure satisfies the following properties,

-almost everywhere, there exists a time such that on and everywhere else.

for each , the distribution of has density

(2)

over the range .

over , is Markov, with transition function of a Brownian motion stopped at zero.

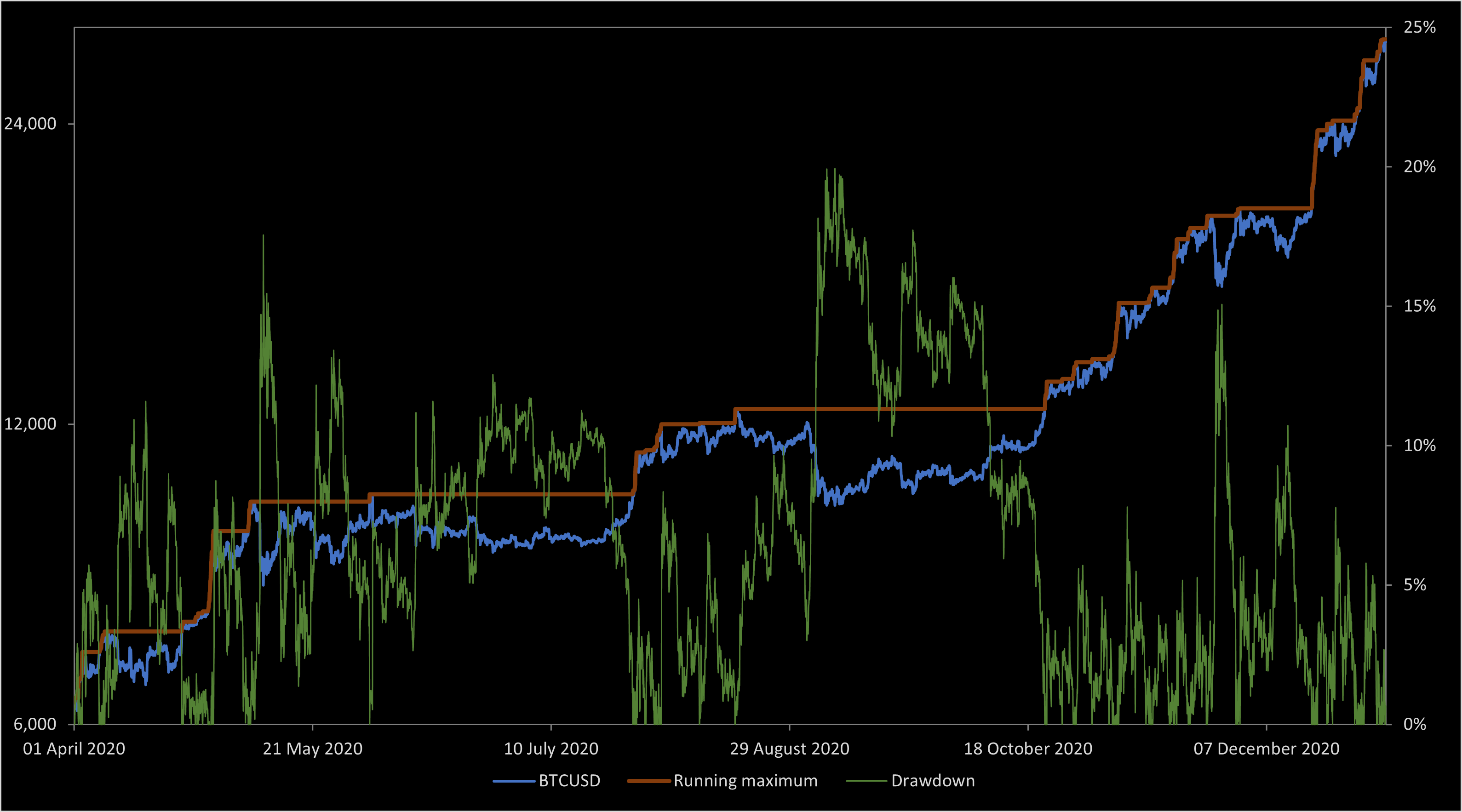

Figure 1: Bitcoin price and drawdown between April and December 2020

For a continuous real-valued stochastic process with running maximum , consider its drawdown. This is just the amount that it has dropped since its maximum so far,

which is a nonnegative process hitting zero whenever the original process visits its running maximum. By looking at each of the individual intervals over which the drawdown is positive, we can break it down into a collection of finite excursions above zero. Furthermore, the running maximum is constant across each of these intervals, so it is natural to index the excursions by this maximum process. By doing so, we obtain a point process. In many cases, it is even a Poisson point process. I look at the drawdown in this post as an example of a point process which is a bit more interesting than the previous example given of the jumps of a cadlag process. By piecing the drawdown excursions back together, it is possible to reconstruct from the point process. At least, this can be done so long as the original process does not monotonically increase over any nontrivial intervals, so that there are no intervals with zero drawdown. As the point process indexes the drawdown by the running maximum, we can also reconstruct X as . The drawdown point process therefore gives an alternative description of our original process.

See figure 1 for the drawdown of the bitcoin price valued in US dollars between April and December 2020. As it makes more sense for this example, the drawdown is shown as a percent of the running maximum, rather than in dollars. This is equivalent to the approach taken in this post applied to the logarithm of the price return over the period, so that . It can be noted that, as the price was mostly increasing, the drawdown consists of a relatively large number of small excursions. If, on the other hand, it had declined, then it would have been dominated by a single large drawdown excursion covering most of the time period.

For simplicity, I will suppose that and that tends to infinity as t goes to infinity. Then, for each , define the random time at which the process first hits level ,

By construction, this is finite, increasing, and left-continuous in . Consider, also, the right limits . Each of the excursions on which the drawdown is positive is equal to one of the intervals . The excursion is defined as a continuous stochastic process equal to the drawdown starting at time and stopped at time ,

This is a continuous nonnegative real-valued process, which starts at zero and is equal to zero at all times after . Note that there uncountably many values for but, the associated excursion will be identically zero other than for the countably many times at which . We will only be interested in these nonzero excursions.

As usual, we work with respect to an underlying probability space , so that we have one path of the stochastic process X defined for each . Associated to this is the collection of drawdown excursions indexed by the running maximum.

As S is defined for each given sample path, it depends on the choice of , so is a countable random set. The sample paths of the excursions lie in the space of continuous functions , which I denote by E. For each time , I use to denote the value of the path sampled at time t,

Use to denote the sigma-algebra on E generated by the collection of maps , so that is the measurable space in which the excursion paths lie. It can be seen that is the Borel sigma-algebra generated by the open subsets of E, with respect to the topology of compact convergence. That is, the topology of uniform convergence on finite time intervals. As this is a complete separable metric space, it makes into a standard Borel space.

Lemma 1 The set S defines a simple point process on ,

for all .

From the definition of point processes, this simply means that is a measurable random variable for each and that there exists a sequence covering E such that are almost surely finite. The set of drawdowns for the point process corresponding to the bitcoin prices in figure 1 are shown in figure 2 below.

Figure 2: Bitcoin price drawdowns between April and December 2020

If S is a finite random set in a standard Borel measurable space satisfying the following two properties,

if are disjoint, then the sizes of and are independent random variables,

for each ,

then it is a Poisson point process. That is, the size of is a Poisson random variable for each . This justifies the use of Poisson point processes in many different areas of probability and stochastic calculus, and provides a convenient method of showing that point processes are indeed Poisson. If the theorem applies, so that we have a Poisson point process, then we just need to compute the intensity measure to fully determine its distribution. The result above was mentioned in the previous post, but I give a precise statement and proof here. Continue reading “Criteria for Poisson Point Processes”→

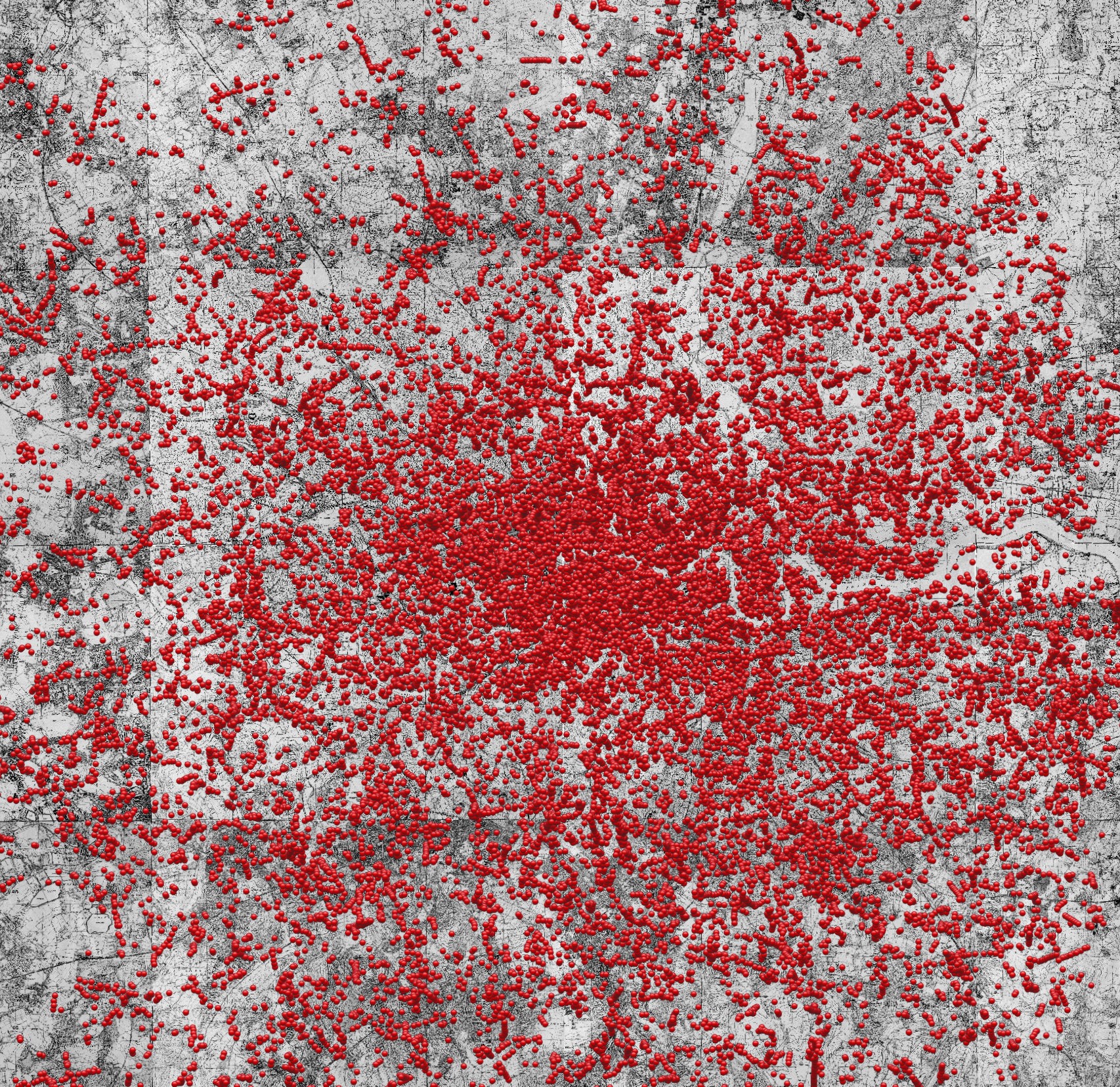

Figure 1: Bomb map of the London Blitz, 7 October 1940 to 6 June 1941. Obtained from http://www.bombsight.org (version 1) on 26 October 2020.

The Poisson distribution models numbers of events that occur in a specific period of time given that, at each instant, whether an event occurs or not is independent of what happens at all other times. Examples which are sometimes cited as candidates for the Poisson distribution include the number of phone calls handled by a telephone exchange on a given day, the number of decays of a radio-active material, and the number of bombs landing in a given area during the London Blitz of 1940-41. The Poisson process counts events which occur according to such distributions.

More generally, the events under consideration need not just happen at specific times, but also at specific locations in a space E. Here, E can represent an actual geometric space in which the events occur, such as the spacial distribution of bombs dropped during the Blitz shown in figure 1, but can also represent other quantities associated with the events. In this example, E could represent the 2-dimensional map of London, or could include both space and time so that where, now, F represents the 2-dimensional map and E is used to record both time and location of the bombs. A Poisson point process is a random set of points in E, such that the number that lie within any measurable subset is Poisson distributed. The aim of this post is to introduce Poisson point processes together with the mathematical machinery to handle such random sets.

The choice of distribution is not arbitrary. Rather, it is a result of the independence of the number of events in each region of the space which leads to the Poisson measure, much like the central limit theorem leads to the ubiquity of the normal distribution for continuous random variables and of Brownian motion for continuous stochastic processes. A random finite subset S of a reasonably ‘nice’ (standard Borel) space E is a Poisson point process so long as it satisfies the properties,

If are pairwise-disjoint measurable subsets of E, then the sizes of are independent.

Individual points of the space each have zero probability of being in S. That is, for each .

The proof of this important result will be given in a later post.

We have come across Poisson point processes previously in my stochastic calculus notes. Specifically, suppose that X is a cadlag -valued stochastic process with independent increments, and which is continuous in probability. Then, the set of points over times t for which the jump is nonzero gives a Poisson point process on . See lemma 4 of the post on processes with independent increments, which corresponds precisely to definition 5 given below. Continue reading “Poisson Point Processes”→

is Poisson with intensity measure

where,

is the standard Lebesgue measure on

.

is a sigma-finite measure on E given by

which vanish on paths of length less than L (some

). The limit is taken over

,

denotes expectation under the measure with respect to which Z is a Brownian motion started at

, and

is the first time at which Z hits 0. This measure satisfies the following properties,

such that

on

and

everywhere else.

, the distribution of

has density

.

![\displaystyle \nu(f) = \lim_{\epsilon\rightarrow0}\epsilon^{-1}{\mathbb E}_\epsilon[f(Z^{\sigma})]](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%5Cnu%28f%29+%3D+%5Clim_%7B%5Cepsilon%5Crightarrow0%7D%5Cepsilon%5E%7B-1%7D%7B%5Cmathbb+E%7D_%5Cepsilon%5Bf%28Z%5E%7B%5Csigma%7D%29%5D+&bg=ffffff&fg=000000&s=0&c=20201002)

with running maximum

with running maximum

from the point process. At least, this can be done so long as the original process does not monotonically increase over any nontrivial intervals, so that there are no intervals with zero drawdown. As the point process indexes the drawdown by the running maximum, we can also reconstruct X as

from the point process. At least, this can be done so long as the original process does not monotonically increase over any nontrivial intervals, so that there are no intervals with zero drawdown. As the point process indexes the drawdown by the running maximum, we can also reconstruct X as  . The drawdown point process therefore gives an alternative description of our original process.

. The drawdown point process therefore gives an alternative description of our original process. . It can be noted that, as the price was mostly increasing, the drawdown consists of a relatively large number of small excursions. If, on the other hand, it had declined, then it would have been dominated by a single large drawdown excursion covering most of the time period.

. It can be noted that, as the price was mostly increasing, the drawdown consists of a relatively large number of small excursions. If, on the other hand, it had declined, then it would have been dominated by a single large drawdown excursion covering most of the time period. and that

and that  tends to infinity as t goes to infinity. Then, for each

tends to infinity as t goes to infinity. Then, for each  , define the random time at which the process first hits level

, define the random time at which the process first hits level

. Each of the excursions on which the drawdown is positive is equal to one of the intervals

. Each of the excursions on which the drawdown is positive is equal to one of the intervals  . The excursion is defined as a continuous stochastic process

. The excursion is defined as a continuous stochastic process  equal to the drawdown starting at time

equal to the drawdown starting at time

. Note that there uncountably many values for

. Note that there uncountably many values for  . We will only be interested in these nonzero excursions.

. We will only be interested in these nonzero excursions. , so that we have one path of the stochastic process X defined for each

, so that we have one path of the stochastic process X defined for each  . Associated to this is the collection of drawdown excursions indexed by the running maximum.

. Associated to this is the collection of drawdown excursions indexed by the running maximum.

, which I denote by E. For each time

, which I denote by E. For each time  , I use

, I use

, so that

, so that  is the measurable space in which the excursion paths lie. It can be seen that

is the measurable space in which the excursion paths lie. It can be seen that  ,

,

.

.  is a measurable random variable for each

is a measurable random variable for each  and that there exists a sequence

and that there exists a sequence  covering E such that

covering E such that  are almost surely finite. The set of drawdowns for the point process corresponding to the bitcoin prices in figure 1 are shown in figure 2 below.

are almost surely finite. The set of drawdowns for the point process corresponding to the bitcoin prices in figure 1 are shown in figure 2 below.

are disjoint, then the sizes of

are disjoint, then the sizes of  and

and  are independent random variables,

are independent random variables, for each

for each  ,

, . This justifies the use of Poisson point processes in many different areas of probability and stochastic calculus, and provides a convenient method of showing that point processes are indeed Poisson. If the theorem applies, so that we have a Poisson point process, then we just need to compute the intensity measure to fully determine its distribution. The result above was mentioned in the previous post, but I give a precise statement and proof here.

. This justifies the use of Poisson point processes in many different areas of probability and stochastic calculus, and provides a convenient method of showing that point processes are indeed Poisson. If the theorem applies, so that we have a Poisson point process, then we just need to compute the intensity measure to fully determine its distribution. The result above was mentioned in the previous post, but I give a precise statement and proof here.

where, now, F represents the 2-dimensional map and E is used to record both time and location of the bombs. A Poisson point process is a random set of points in E, such that the number that lie within any measurable subset is Poisson distributed. The aim of this post is to introduce Poisson point processes together with the mathematical machinery to handle such random sets.

where, now, F represents the 2-dimensional map and E is used to record both time and location of the bombs. A Poisson point process is a random set of points in E, such that the number that lie within any measurable subset is Poisson distributed. The aim of this post is to introduce Poisson point processes together with the mathematical machinery to handle such random sets. are pairwise-disjoint measurable subsets of E, then the sizes of

are pairwise-disjoint measurable subsets of E, then the sizes of  are independent.

are independent. -valued stochastic process with independent increments, and which is continuous in probability. Then, the set of points

-valued stochastic process with independent increments, and which is continuous in probability. Then, the set of points  over times t for which the jump

over times t for which the jump  is nonzero gives a Poisson point process on

is nonzero gives a Poisson point process on  . See lemma

. See lemma