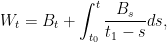

Consider a stochastic process X of the form

|

(1) |

for a standard Brownian motion W and predictable process  , defined with respect to a filtered probability space

, defined with respect to a filtered probability space  . For this to make sense, we must assume that

. For this to make sense, we must assume that  is almost surely finite at all times, and I will suppose that

is almost surely finite at all times, and I will suppose that  is the filtration generated by W.

is the filtration generated by W.

The question is whether the drift can be backed out from knowledge of the process X alone. As I will show with an example, this is not possible. In fact, in our example, X will itself be a standard Brownian motion, even though the drift is non-trivial (that is,  is not almost surely zero). In this case X has exactly the same distribution as W, so cannot be distinguished from the driftless case with

is not almost surely zero). In this case X has exactly the same distribution as W, so cannot be distinguished from the driftless case with  by looking at the distribution of X alone.

by looking at the distribution of X alone.

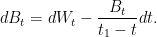

On the face of it, this seems rather counter-intuitive. By standard semimartingale decomposition, it is known that we can always decompose

|

(2) |

for a unique continuous local martingale M starting from zero, and unique continuous FV process A. By uniqueness,  and

and  . This allows us to back out the drift and, in particular, if the drift is non-trivial then X cannot be a martingale. However, in the semimartingale decomposition, it is required that M is a martingale with respect to the original filtration . If we do not know the filtration , then it might not be possible to construct decomposition (2) from knowledge of X alone. As mentioned above, we will give an example where X is a standard Brownian motion which, in particular, means that it is a martingale under its natural filtration. By the semimartingale decomposition result, it is not possible for X to be an -martingale. A consequence of this is that the natural filtration of X must be strictly smaller than the natural filtration of W.

. This allows us to back out the drift and, in particular, if the drift is non-trivial then X cannot be a martingale. However, in the semimartingale decomposition, it is required that M is a martingale with respect to the original filtration . If we do not know the filtration , then it might not be possible to construct decomposition (2) from knowledge of X alone. As mentioned above, we will give an example where X is a standard Brownian motion which, in particular, means that it is a martingale under its natural filtration. By the semimartingale decomposition result, it is not possible for X to be an -martingale. A consequence of this is that the natural filtration of X must be strictly smaller than the natural filtration of W.

The inspiration for this post was a comment by Gabe posing the following question: If we take  to be the filtration generated by a standard Brownian motion W in

to be the filtration generated by a standard Brownian motion W in  , and we define

, and we define  , can we find an -adapted

, can we find an -adapted  such that the filtration generated by

such that the filtration generated by  is smaller than ? Our example gives an affirmative answer.

is smaller than ? Our example gives an affirmative answer.

Brownian Bridge Construction

The example of a process with hidden drift will be based around the decomposition of a Brownian motion into Brownian bridges or, conversely, the composition of a standard Brownian motion from Brownian bridges. So, I first quickly go over this standard material.

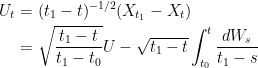

Let us start with a Brownian motion  defined over an interval

defined over an interval ![{[t_0,t_1]}](https://s0.wp.com/latex.php?latex=%7B%5Bt_0%2Ct_1%5D%7D&bg=ffffff&fg=000000&s=0&c=20201002) . We consider the linear interpolant across the interval,

. We consider the linear interpolant across the interval,

and the deviation of the process from this interpolation,

It can be seen that B is independent of X at the interval endpoints. It is straightforward to compute the covariances of  and

and  , which are zero. As the increments of X are jointly normal, independence follows. In fact, B is a Brownian bridge. The process

, which are zero. As the increments of X are jointly normal, independence follows. In fact, B is a Brownian bridge. The process

is a Brownian motion over which, again, can be shown by computing covariances. Differentiating, the Brownian bridge B is given from the Brownian motion W via the SDE

This can be solved to express B in terms of W,

|

(3) |

Now, suppose we are given the following, for times  , defined on the same probability space.

, defined on the same probability space.

- A random variable

.

.

- A standard normal random variable

.

.

- A Brownian motion

over the interval .

over the interval .

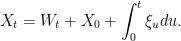

We furthermore suppose that , U and W are independent. The idea is to construct a new Brownian motion X on the interval . Taking as specified, we need  to be normal with variance

to be normal with variance  . This is done by setting

. This is done by setting

We interpolate X across the interval by inverting the Brownian bridge decomposition above. Constructing a Brownian bridge by (3) and adding this to the linear interpolation of X gives

|

(4) |

for all times  . This is our desired Brownian motion. Expressing things slightly differently, we have

. This is our desired Brownian motion. Expressing things slightly differently, we have

|

(5) |

where is the process

|

(6) |

I will also note that, as standard Brownian motion has independent normal increments, for any fixed time ![{t\in[t_0,t_1]}](https://s0.wp.com/latex.php?latex=%7Bt%5Cin%5Bt_0%2Ct_1%5D%7D&bg=ffffff&fg=000000&s=0&c=20201002) the random variable

the random variable

|

(7) |

will be standard normal and independent of  over

over  .

.

Solution to the Hidden Drift Problem

We assume are given a standard Brownian motion W. Start by choosing a strictly increasing sequence of positive times  such that

such that  as

as  and

and  as

as  . For example, we can simply take

. For example, we can simply take  .

.

Setting  , we have an infinite sequence of overlapping intervals

, we have an infinite sequence of overlapping intervals ![{[t_{n-1},t^\prime_n]}](https://s0.wp.com/latex.php?latex=%7B%5Bt_%7Bn-1%7D%2Ct%5E%5Cprime_n%5D%7D&bg=ffffff&fg=000000&s=0&c=20201002) containing

containing  in their interiors. The idea is to use the Brownian Bridge construction described above to construct X across each of these intervals. To do this, for each n, we need to construct a standard normal random variable

in their interiors. The idea is to use the Brownian Bridge construction described above to construct X across each of these intervals. To do this, for each n, we need to construct a standard normal random variable  which is independent of

which is independent of  . Given that we have already applied the above construction across the interval

. Given that we have already applied the above construction across the interval ![{[t_{n-1},t_n^\prime]}](https://s0.wp.com/latex.php?latex=%7B%5Bt_%7Bn-1%7D%2Ct_n%5E%5Cprime%5D%7D&bg=ffffff&fg=000000&s=0&c=20201002) , starting with a standard normal

, starting with a standard normal  , we can construct the new standard normal with the required independence property by (7),

, we can construct the new standard normal with the required independence property by (7),

|

(8) |

Since  , we can solve this recursive formula as

, we can solve this recursive formula as

for any  . Noting that

. Noting that  as

as  , we can take the limit to obtain

, we can take the limit to obtain

|

(9) |

I take (9) as the definition of , which we note are a sequence of standard normal random variables satisfying (8), and that is  -measurable. Next, we define X across the interval

-measurable. Next, we define X across the interval ![{[t_{n-1},t_n]\subseteq[t_{n-1},t^\prime_n]}](https://s0.wp.com/latex.php?latex=%7B%5Bt_%7Bn-1%7D%2Ct_n%5D%5Csubseteq%5Bt_%7Bn-1%7D%2Ct%5E%5Cprime_n%5D%7D&bg=ffffff&fg=000000&s=0&c=20201002) so that it obeys (4) above,

so that it obeys (4) above,

From the construction above, this ensures that is independent of the increments of over , and that X is a standard Brownian motion. From (5) and (6), we obtain

|

(10) |

for all times  , with the drift process

, with the drift process

|

(11) |

over  . In order to take the limit

. In order to take the limit  in (10), we need to show that

in (10), we need to show that  is almost surely finite. From (11),

is almost surely finite. From (11),  is standard normal with variance

is standard normal with variance  and, hence,

and, hence, ![{{\mathbb E}[\lvert\xi_t\rvert]=\sqrt{2/\pi(t^\prime_n-t)}}](https://s0.wp.com/latex.php?latex=%7B%7B%5Cmathbb+E%7D%5B%5Clvert%5Cxi_t%5Crvert%5D%3D%5Csqrt%7B2%2F%5Cpi%28t%5E%5Cprime_n-t%29%7D%7D&bg=ffffff&fg=000000&s=0&c=20201002) giving,

giving,

![\displaystyle \setlength\arraycolsep{2pt} \begin{array}{rl} \displaystyle {\mathbb E}\left[\int_0^{t_n}\lvert\xi_t\rvert dt\right] &\displaystyle =\int_0^{t_n}{\mathbb E}[\lvert\xi_t\rvert]dt =\sqrt{\frac2\pi}\sum_{m=-\infty}^n\int_{t_{m-1}}^{t_m}(t_m^\prime-t)^{-1/2}dt\smallskip\\ &\displaystyle =\sqrt{\frac8\pi}\sum_{m=-\infty}^n\left(\sqrt{t^\prime_m-t_{m-1}}-\sqrt{t^\prime_m-t_m}\right)\smallskip\\ &\displaystyle =(\sqrt2-1)\sqrt{\frac8\pi}\sum_{m=-\infty}^n\sqrt{t_m-t_{m-1}} \end{array}](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%5Csetlength%5Carraycolsep%7B2pt%7D+%5Cbegin%7Barray%7D%7Brl%7D+%5Cdisplaystyle+%7B%5Cmathbb+E%7D%5Cleft%5B%5Cint_0%5E%7Bt_n%7D%5Clvert%5Cxi_t%5Crvert+dt%5Cright%5D+%26%5Cdisplaystyle+%3D%5Cint_0%5E%7Bt_n%7D%7B%5Cmathbb+E%7D%5B%5Clvert%5Cxi_t%5Crvert%5Ddt+%3D%5Csqrt%7B%5Cfrac2%5Cpi%7D%5Csum_%7Bm%3D-%5Cinfty%7D%5En%5Cint_%7Bt_%7Bm-1%7D%7D%5E%7Bt_m%7D%28t_m%5E%5Cprime-t%29%5E%7B-1%2F2%7Ddt%5Csmallskip%5C%5C+%26%5Cdisplaystyle+%3D%5Csqrt%7B%5Cfrac8%5Cpi%7D%5Csum_%7Bm%3D-%5Cinfty%7D%5En%5Cleft%28%5Csqrt%7Bt%5E%5Cprime_m-t_%7Bm-1%7D%7D-%5Csqrt%7Bt%5E%5Cprime_m-t_m%7D%5Cright%29%5Csmallskip%5C%5C+%26%5Cdisplaystyle+%3D%28%5Csqrt2-1%29%5Csqrt%7B%5Cfrac8%5Cpi%7D%5Csum_%7Bm%3D-%5Cinfty%7D%5En%5Csqrt%7Bt_m-t_%7Bm-1%7D%7D+%5Cend%7Barray%7D+&bg=ffffff&fg=000000&s=0&c=20201002)

So long as  is finite, this guarantees that is almost surely finite. This is true for the simple case with and, hence, we can take the limit in (10) to obtain

is finite, this guarantees that is almost surely finite. This is true for the simple case with and, hence, we can take the limit in (10) to obtain

Choose  giving (1) as required.

giving (1) as required.

I finally note that the original motivation for this example was to find a process X satisfying (1) whose natural filtration is strictly smaller than that of W. Letting  be the filtration generated by X, we see that is -measurable but is independent of

be the filtration generated by X, we see that is -measurable but is independent of  , directly demonstrating that

, directly demonstrating that  .

.