Ito’s lemma is one of the most important and useful results in the theory of stochastic calculus. This is a stochastic generalization of the chain rule, or change of variables formula, and differs from the classical deterministic formulas by the presence of a quadratic variation term. One drawback which can limit the applicability of Ito’s lemma in some situations, is that it only applies for twice continuously differentiable functions. However, the quadratic variation term can alternatively be expressed using local times, which relaxes the differentiability requirement. This generalization of Ito’s lemma was derived by Tanaka and Meyer, and applies to one dimensional semimartingales.

The local time of a stochastic process X at a fixed level x can be written, very informally, as an integral of a Dirac delta function with respect to the continuous part of the quadratic variation ![{[X]^{c}}](https://s0.wp.com/latex.php?latex=%7B%5BX%5D%5E%7Bc%7D%7D&bg=ffffff&fg=000000&s=0&c=20201002) ,

,

![\displaystyle L^x_t=\int_0^t\delta(X-x)d[X]^c.](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++L%5Ex_t%3D%5Cint_0%5Et%5Cdelta%28X-x%29d%5BX%5D%5Ec.+&bg=ffffff&fg=000000&s=0&c=20201002) |

(1) |

This was explained in an earlier post. As the Dirac delta is only a distribution, and not a true function, equation (1) is not really a well-defined mathematical expression. However, as we saw, with some manipulation a valid expression can be obtained which defines the local time whenever X is a semimartingale.

Going in a slightly different direction, we can try multiplying (1) by a bounded measurable function  and integrating over x. Commuting the order of integration on the right hand side, and applying the defining property of the delta function, that

and integrating over x. Commuting the order of integration on the right hand side, and applying the defining property of the delta function, that  is equal to

is equal to  , gives

, gives

![\displaystyle \int_{-\infty}^{\infty} L^x_t f(x)dx=\int_0^tf(X)d[X]^c.](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%5Cint_%7B-%5Cinfty%7D%5E%7B%5Cinfty%7D+L%5Ex_t+f%28x%29dx%3D%5Cint_0%5Etf%28X%29d%5BX%5D%5Ec.+&bg=ffffff&fg=000000&s=0&c=20201002) |

(2) |

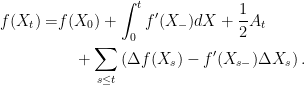

By eliminating the delta function, the right hand side has been transformed into a well-defined expression. In fact, it is now the left side of the identity that is a problem, since the local time was only defined up to probability one at each level x. Ignoring this issue for the moment, recall the version of Ito’s lemma for general non-continuous semimartingales,

|

(3) |

where ![{A_t=\int_0^t f^{\prime\prime}(X)d[X]^c}](https://s0.wp.com/latex.php?latex=%7BA_t%3D%5Cint_0%5Et+f%5E%7B%5Cprime%5Cprime%7D%28X%29d%5BX%5D%5Ec%7D&bg=ffffff&fg=000000&s=0&c=20201002) . Equation (2) allows us to express this quadratic variation term using local times,

. Equation (2) allows us to express this quadratic variation term using local times,

The benefit of this form is that, even though it still uses the second derivative of  , it is only really necessary for this to exist in a weaker, measure theoretic, sense. Suppose that is convex, or a linear combination of convex functions. Then, its right-hand derivative

, it is only really necessary for this to exist in a weaker, measure theoretic, sense. Suppose that is convex, or a linear combination of convex functions. Then, its right-hand derivative  exists, and is itself of locally finite variation. Hence, the Stieltjes integral

exists, and is itself of locally finite variation. Hence, the Stieltjes integral  exists. The infinitesimal

exists. The infinitesimal  is alternatively written

is alternatively written  and, in the twice continuously differentiable case, equals

and, in the twice continuously differentiable case, equals  . Then,

. Then,

|

(4) |

Using this expression in (3) gives the Ito-Tanaka-Meyer formula. Continue reading “The Ito-Tanaka-Meyer Formula” →

-Hölder continuous w.r.t. x, for all

and over all bounded regions for t.

is a measure of the time spent at x. For a continuous time stochastic process, we could try and simply compute the Lebesgue measure of the time at the level,

is a measure of the time spent at x. For a continuous time stochastic process, we could try and simply compute the Lebesgue measure of the time at the level,

and stick there for some time, this makes some sense. However, if X is a standard

and stick there for some time, this makes some sense. However, if X is a standard  at each positive time, so that that

at each positive time, so that that  defined by (

defined by ( as in (

as in (

![{{\mathbb E}[\delta(X_s-x)]}](https://s0.wp.com/latex.php?latex=%7B%7B%5Cmathbb+E%7D%5B%5Cdelta%28X_s-x%29%5D%7D&bg=ffffff&fg=000000&s=0&c=20201002) can be interpreted as the probability density of

can be interpreted as the probability density of  evaluated at

evaluated at ![\displaystyle L^x_t=\int_0^t\delta(X_s-x)d[X]_s](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++L%5Ex_t%3D%5Cint_0%5Et%5Cdelta%28X_s-x%29d%5BX%5D_s+&bg=ffffff&fg=000000&s=0&c=20201002)

![{\int f^{\prime\prime}(X)d[X]}](https://s0.wp.com/latex.php?latex=%7B%5Cint+f%5E%7B%5Cprime%5Cprime%7D%28X%29d%5BX%5D%7D&bg=ffffff&fg=000000&s=0&c=20201002) and, hence, requires

and, hence, requires  can be understood in terms of distributions, and delta functions can appear, which brings local times into the picture. In the opposite direction, which I take in this post, we can try to generalise Ito’s formula and invert this to give a meaning to (

can be understood in terms of distributions, and delta functions can appear, which brings local times into the picture. In the opposite direction, which I take in this post, we can try to generalise Ito’s formula and invert this to give a meaning to (