Being able to handle quadratic variations and covariations of processes is very important in stochastic calculus. Apart from appearing in the integration by parts formula, they are required for the stochastic change of variables formula, known as Ito’s lemma, which will be the subject of the next post. Quadratic covariations satisfy several simple relations which make them easy to handle, especially in conjunction with the stochastic integral.

Recall from the previous post that the covariation ![{[X,Y]}](https://s0.wp.com/latex.php?latex=%7B%5BX%2CY%5D%7D&bg=ffffff&fg=000000&s=0&c=20201002)

![{\Delta [X,Y]_t\equiv [X,Y]_t-[X,Y]_{t-}}](https://s0.wp.com/latex.php?latex=%7B%5CDelta+%5BX%2CY%5D_t%5Cequiv+%5BX%2CY%5D_t-%5BX%2CY%5D_%7Bt-%7D%7D&bg=ffffff&fg=000000&s=0&c=20201002)

Lemma 1 If

are semimartingales then

(1) In particular,

.

![\displaystyle \Delta [X,Y]=\Delta X\Delta Y.](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%5CDelta+%5BX%2CY%5D%3D%5CDelta+X%5CDelta+Y.+&bg=ffffff&fg=000000&s=0&c=20201002)

Proof: Taking the jumps of the integration by parts formula for

![\displaystyle \Delta XY = X_{-}\Delta Y + Y_{-}\Delta X + \Delta [X,Y],](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%5CDelta+XY+%3D+X_%7B-%7D%5CDelta+Y+%2B+Y_%7B-%7D%5CDelta+X+%2B+%5CDelta+%5BX%2CY%5D%2C+&bg=ffffff&fg=000000&s=0&c=20201002) |

and rearranging this gives the result. ⬜

An immediate consequence is that quadratic variations and covariations involving continuous processes are continuous. Another consequence is that the sum of the squares of the jumps of a semimartingale over any bounded interval must be finite.

Corollary 2 Every semimartingale

satisfies

![\displaystyle \sum_{s\le t}\Delta X^2_s\le [X]_t<\infty.](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%5Csum_%7Bs%5Cle+t%7D%5CDelta+X%5E2_s%5Cle+%5BX%5D_t%3C%5Cinfty.+&bg=ffffff&fg=000000&s=0&c=20201002)

Proof: As ![{[X]}](https://s0.wp.com/latex.php?latex=%7B%5BX%5D%7D&bg=ffffff&fg=000000&s=0&c=20201002)

![{[X]_t\ge \sum_{s\le t}\Delta [X]_s}](https://s0.wp.com/latex.php?latex=%7B%5BX%5D_t%5Cge+%5Csum_%7Bs%5Cle+t%7D%5CDelta+%5BX%5D_s%7D&bg=ffffff&fg=000000&s=0&c=20201002)

![{\Delta[X]=\Delta X^2}](https://s0.wp.com/latex.php?latex=%7B%5CDelta%5BX%5D%3D%5CDelta+X%5E2%7D&bg=ffffff&fg=000000&s=0&c=20201002)

Next, the following result shows that covariations involving continuous finite variation processes are zero. As Lebesgue-Stieltjes integration is only defined for finite variation processes, this shows why quadratic variations do not play an important role in standard calculus. For noncontinuous finite variation processes, the covariation must have jumps satisfying (1), so will generally be nonzero. In this case, the covariation is just given by the sum over these jumps. Integration with respect to any FV process

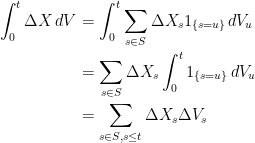

Lemma 3 Let

(2) In particular, if either of

.

![\displaystyle [X,V]_t = \int_0^t \Delta X\,dV = \sum_{s\le t}\Delta X_s\Delta V_s.](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%5BX%2CV%5D_t+%3D+%5Cint_0%5Et+%5CDelta+X%5C%2CdV+%3D+%5Csum_%7Bs%5Cle+t%7D%5CDelta+X_s%5CDelta+V_s.+&bg=ffffff&fg=000000&s=0&c=20201002)

Proof: Expressing the covariation as the limit along equally spaced partitions of ![{[0,t]}](https://s0.wp.com/latex.php?latex=%7B%5B0%2Ct%5D%7D&bg=ffffff&fg=000000&s=0&c=20201002)

![\displaystyle \setlength\arraycolsep{2pt} \begin{array}{rl} \displaystyle [X,V]_t &\displaystyle= \lim_{n\rightarrow\infty}\sum_{k=1}^n (X_{kt/n}-X_{(k-1)t/n})(V_{kt/n}-V_{(k-1)t/n})\smallskip\\ &\displaystyle=\lim_{n\rightarrow\infty}\sum_{k=1}^n\int_0^t 1_{\{(k-1)t/n<s\le kt/n\}}(X_{kt/n}-X_{(k-1)t/n})\,dV_s\smallskip\\ &\displaystyle=\int_0^t\lim_{n\rightarrow\infty}\sum_{k=1}^n 1_{\{(k-1)t/n<s\le kt/n\}}(X_{kt/n}-X_{(k-1)t/n})\,dV_s\smallskip\\ &\displaystyle=\int_0^t\Delta X_s\,dV_s. \end{array}](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%5Csetlength%5Carraycolsep%7B2pt%7D+%5Cbegin%7Barray%7D%7Brl%7D+%5Cdisplaystyle+%5BX%2CV%5D_t+%26%5Cdisplaystyle%3D+%5Clim_%7Bn%5Crightarrow%5Cinfty%7D%5Csum_%7Bk%3D1%7D%5En+%28X_%7Bkt%2Fn%7D-X_%7B%28k-1%29t%2Fn%7D%29%28V_%7Bkt%2Fn%7D-V_%7B%28k-1%29t%2Fn%7D%29%5Csmallskip%5C%5C+%26%5Cdisplaystyle%3D%5Clim_%7Bn%5Crightarrow%5Cinfty%7D%5Csum_%7Bk%3D1%7D%5En%5Cint_0%5Et+1_%7B%5C%7B%28k-1%29t%2Fn%3Cs%5Cle+kt%2Fn%5C%7D%7D%28X_%7Bkt%2Fn%7D-X_%7B%28k-1%29t%2Fn%7D%29%5C%2CdV_s%5Csmallskip%5C%5C+%26%5Cdisplaystyle%3D%5Cint_0%5Et%5Clim_%7Bn%5Crightarrow%5Cinfty%7D%5Csum_%7Bk%3D1%7D%5En+1_%7B%5C%7B%28k-1%29t%2Fn%3Cs%5Cle+kt%2Fn%5C%7D%7D%28X_%7Bkt%2Fn%7D-X_%7B%28k-1%29t%2Fn%7D%29%5C%2CdV_s%5Csmallskip%5C%5C+%26%5Cdisplaystyle%3D%5Cint_0%5Et%5CDelta+X_s%5C%2CdV_s.+%5Cend%7Barray%7D+&bg=ffffff&fg=000000&s=0&c=20201002) |

The third equality here makes use of the bounded convergence theorem to commute the limit with the integral sign. Then, as

|

as required. ⬜

If

![\displaystyle [X+V,Y+W]=[X,Y].](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%5BX%2BV%2CY%2BW%5D%3D%5BX%2CY%5D.+&bg=ffffff&fg=000000&s=0&c=20201002) |

That is, when calculating covariations, we can disregard any continuous FV terms added to the processes. A consequence of Lemma 3 is that the standard integration by parts formula, with no covariation term, applies whenever either of the two processes has finite variation. The integral with respect to the FV process

Corollary 4 Let

Proof: Substitute (2) for the covariation term in the integration by parts formula to get the following

|

The final two integrals on the right hand side can be combined into a single integral of

A d-dimensional process

![\displaystyle [X]^{ij}\equiv [X^i,X^j].](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%5BX%5D%5E%7Bij%7D%5Cequiv+%5BX%5Ei%2CX%5Ej%5D.+&bg=ffffff&fg=000000&s=0&c=20201002) |

This will also be increasing, in the sense that ![{[X]_t-[X]_s}](https://s0.wp.com/latex.php?latex=%7B%5BX%5D_t-%5BX%5D_s%7D&bg=ffffff&fg=000000&s=0&c=20201002)

![\displaystyle \lambda^{\rm t}[X]\lambda = \lambda^i\lambda^j[X^i,X^j]=\left[\lambda\cdot X\right]](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%5Clambda%5E%7B%5Crm+t%7D%5BX%5D%5Clambda+%3D+%5Clambda%5Ei%5Clambda%5Ej%5BX%5Ei%2CX%5Ej%5D%3D%5Cleft%5B%5Clambda%5Ccdot+X%5Cright%5D+&bg=ffffff&fg=000000&s=0&c=20201002) |

is increasing for all vectors

Lemma 5 Let

be semimartingales and

be bounded and measurable processes. Then,

(3) is an increasing process.

![\displaystyle \int \xi^i\xi^j\,d[X^i,X^j]](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%5Cint+%5Cxi%5Ei%5Cxi%5Ej%5C%2Cd%5BX%5Ei%2CX%5Ej%5D+&bg=ffffff&fg=000000&s=0&c=20201002)

Proof: Almost surely,

|

(4) |

for

![\displaystyle \setlength\arraycolsep{2pt} \begin{array}{rl} \displaystyle\int_0^t \xi^i\xi^j\,d[X^i,X^j] &\displaystyle= \sum_{k=1}^n \int_0^t 1_{\{t_{k-1}<s\le t_{k-1}\}}c^i_kc^j_k\,d[X^i,X^j]_s\smallskip\\ &\displaystyle=\sum_{k=1}^n c^{\rm t}_k([X]_{t\wedge t_k}-[X]_{t\wedge t_{k-1}})c_k \end{array}](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%5Csetlength%5Carraycolsep%7B2pt%7D+%5Cbegin%7Barray%7D%7Brl%7D+%5Cdisplaystyle%5Cint_0%5Et+%5Cxi%5Ei%5Cxi%5Ej%5C%2Cd%5BX%5Ei%2CX%5Ej%5D+%26%5Cdisplaystyle%3D+%5Csum_%7Bk%3D1%7D%5En+%5Cint_0%5Et+1_%7B%5C%7Bt_%7Bk-1%7D%3Cs%5Cle+t_%7Bk-1%7D%5C%7D%7Dc%5Ei_kc%5Ej_k%5C%2Cd%5BX%5Ei%2CX%5Ej%5D_s%5Csmallskip%5C%5C+%26%5Cdisplaystyle%3D%5Csum_%7Bk%3D1%7D%5En+c%5E%7B%5Crm+t%7D_k%28%5BX%5D_%7Bt%5Cwedge+t_k%7D-%5BX%5D_%7Bt%5Cwedge+t_%7Bk-1%7D%7D%29c_k+%5Cend%7Barray%7D+&bg=ffffff&fg=000000&s=0&c=20201002) |

which is increasing. The idea is to apply the functional monotone class theorem to extend this to all bounded and measurable processes. So, let

The quadratic covariation considered as a bilinear map ![{(X,Y)\mapsto [X,Y]_t}](https://s0.wp.com/latex.php?latex=%7B%28X%2CY%29%5Cmapsto+%5BX%2CY%5D_t%7D&bg=ffffff&fg=000000&s=0&c=20201002)

![\displaystyle \vert [X,Y]\vert \le\sqrt{[X][Y]}](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%5Cvert+%5BX%2CY%5D%5Cvert+%5Cle%5Csqrt%7B%5BX%5D%5BY%5D%7D+&bg=ffffff&fg=000000&s=0&c=20201002) |

More generally, the previous result can be used to obtain the Kunita-Watanabe inequality.

Theorem 6 (Kunita-Watanabe Inequality) Let

be measurable processes. Then,

![\displaystyle \int_0^t\vert\alpha\beta\vert\,\vert d[X,Y]\vert\le\sqrt{\int_0^t\alpha^2\,d[X]\,\int_0^t\beta^2\,d[Y]}.](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%5Cint_0%5Et%5Cvert%5Calpha%5Cbeta%5Cvert%5C%2C%5Cvert+d%5BX%2CY%5D%5Cvert%5Cle%5Csqrt%7B%5Cint_0%5Et%5Calpha%5E2%5C%2Cd%5BX%5D%5C%2C%5Cint_0%5Et%5Cbeta%5E2%5C%2Cd%5BY%5D%7D.+&bg=ffffff&fg=000000&s=0&c=20201002)

Proof: First, suppose that

![\displaystyle \lambda^2\int\alpha^2\,d[X]+\int\beta^2\,d[Y]\pm 2\lambda\int\alpha\beta\,d[X,Y]](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%5Clambda%5E2%5Cint%5Calpha%5E2%5C%2Cd%5BX%5D%2B%5Cint%5Cbeta%5E2%5C%2Cd%5BY%5D%5Cpm+2%5Clambda%5Cint%5Calpha%5Cbeta%5C%2Cd%5BX%2CY%5D+&bg=ffffff&fg=000000&s=0&c=20201002) |

is an increasing process. As the first two terms are increasing, and the variation of the third term is ![{2\lambda\int\vert\alpha\beta\vert\,\vert d[X,Y]\vert}](https://s0.wp.com/latex.php?latex=%7B2%5Clambda%5Cint%5Cvert%5Calpha%5Cbeta%5Cvert%5C%2C%5Cvert+d%5BX%2CY%5D%5Cvert%7D&bg=ffffff&fg=000000&s=0&c=20201002)

![\displaystyle 2\lambda\int_0^t\vert\alpha\beta\vert\,\vert d[X,Y]\vert\le \lambda^2\int_0^t\alpha^2\,d[X]+\int_0^t\beta^2\,d[Y].](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++2%5Clambda%5Cint_0%5Et%5Cvert%5Calpha%5Cbeta%5Cvert%5C%2C%5Cvert+d%5BX%2CY%5D%5Cvert%5Cle+%5Clambda%5E2%5Cint_0%5Et%5Calpha%5E2%5C%2Cd%5BX%5D%2B%5Cint_0%5Et%5Cbeta%5E2%5C%2Cd%5BY%5D.+&bg=ffffff&fg=000000&s=0&c=20201002) |

The result follows by setting ![{\lambda=(\int_0^t\alpha^2\,d[X])^{-1/2}(\int_0^t\beta^2\,d[Y])^{1/2}}](https://s0.wp.com/latex.php?latex=%7B%5Clambda%3D%28%5Cint_0%5Et%5Calpha%5E2%5C%2Cd%5BX%5D%29%5E%7B-1%2F2%7D%28%5Cint_0%5Et%5Cbeta%5E2%5C%2Cd%5BY%5D%29%5E%7B1%2F2%7D%7D&bg=ffffff&fg=000000&s=0&c=20201002)

For example, consider standard Brownian motions

![{[B^1]_t=[B^2]_t=t}](https://s0.wp.com/latex.php?latex=%7B%5BB%5E1%5D_t%3D%5BB%5E2%5D_t%3Dt%7D&bg=ffffff&fg=000000&s=0&c=20201002)

![\displaystyle \int\xi^2\,\vert d[B^1,B^2]\vert \le \int\xi^2\,dt.](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%5Cint%5Cxi%5E2%5C%2C%5Cvert+d%5BB%5E1%2CB%5E2%5D%5Cvert+%5Cle+%5Cint%5Cxi%5E2%5C%2Cdt.+&bg=ffffff&fg=000000&s=0&c=20201002) |

The Radon-Nikodym theorem can then be used to imply the existence of a predictable process

![{d[B^1,B^2]=\rho\,dt}](https://s0.wp.com/latex.php?latex=%7Bd%5BB%5E1%2CB%5E2%5D%3D%5Crho%5C%2Cdt%7D&bg=ffffff&fg=000000&s=0&c=20201002)

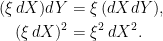

We now arrive at the following result allowing us to commute the order in which stochastic integrals and quadratic covariations are calculated. This is a very useful result which is often required when manipulating stochastic integrals. Note that equations (6) and (7) can be written in differential form as follows,

|

Theorem 7 Let

(5) and,

(6) Furthermore, the quadratic variation of

is given by,

(7)

![\displaystyle \int_0^t\vert\xi\vert\,\vert d[X,Y]\vert<\infty](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%5Cint_0%5Et%5Cvert%5Cxi%5Cvert%5C%2C%5Cvert+d%5BX%2CY%5D%5Cvert%3C%5Cinfty+&bg=ffffff&fg=000000&s=0&c=20201002)

![\displaystyle \left[\int\xi\,dX,Y\right] = \int\xi\,d[X,Y].](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%5Cleft%5B%5Cint%5Cxi%5C%2CdX%2CY%5Cright%5D+%3D+%5Cint%5Cxi%5C%2Cd%5BX%2CY%5D.+&bg=ffffff&fg=000000&s=0&c=20201002)

![\displaystyle \left[\int\xi\,dX\right]=\int\xi^2\,d[X].](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%5Cleft%5B%5Cint%5Cxi%5C%2CdX%5Cright%5D%3D%5Cint%5Cxi%5E2%5C%2Cd%5BX%5D.+&bg=ffffff&fg=000000&s=0&c=20201002)

As an example, consider Ito processes

|

where

![\displaystyle d[X,Y] = (\alpha\,dB^1)(\beta\,dB^2)=\alpha\beta\,dB^1dB^2 = \alpha\beta\rho\,dt.](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++d%5BX%2CY%5D+%3D+%28%5Calpha%5C%2CdB%5E1%29%28%5Cbeta%5C%2CdB%5E2%29%3D%5Calpha%5Cbeta%5C%2CdB%5E1dB%5E2+%3D+%5Calpha%5Cbeta%5Crho%5C%2Cdt.+&bg=ffffff&fg=000000&s=0&c=20201002) |

The proof of Theorem 7 is as follows.

Proof: First, consider the case where

![{(s,t]}](https://s0.wp.com/latex.php?latex=%7B%28s%2Ct%5D%7D&bg=ffffff&fg=000000&s=0&c=20201002)

![\displaystyle \setlength\arraycolsep{2pt} \begin{array}{rl} \displaystyle [Z,Y]^P_t &\displaystyle= \sum_{n=1}^\infty (Z_{\tau_n\wedge t}-Z_{\tau_{n-1}\wedge t})(Y_{\tau_n\wedge t}-Y_{\tau_{n-1}\wedge t})\smallskip\\ &\displaystyle=\sum_{n=1}^\infty \xi_{\tau_n}(X_{\tau_n\wedge t}-X_{\tau_{n-1}\wedge t})(Y_{\tau_n\wedge t}-Y_{\tau_{n-1}\wedge t})\smallskip\\ &\displaystyle=\int_0^t\xi\,d[X,Y]^P. \end{array}](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%5Csetlength%5Carraycolsep%7B2pt%7D+%5Cbegin%7Barray%7D%7Brl%7D+%5Cdisplaystyle+%5BZ%2CY%5D%5EP_t+%26%5Cdisplaystyle%3D+%5Csum_%7Bn%3D1%7D%5E%5Cinfty+%28Z_%7B%5Ctau_n%5Cwedge+t%7D-Z_%7B%5Ctau_%7Bn-1%7D%5Cwedge+t%7D%29%28Y_%7B%5Ctau_n%5Cwedge+t%7D-Y_%7B%5Ctau_%7Bn-1%7D%5Cwedge+t%7D%29%5Csmallskip%5C%5C+%26%5Cdisplaystyle%3D%5Csum_%7Bn%3D1%7D%5E%5Cinfty+%5Cxi_%7B%5Ctau_n%7D%28X_%7B%5Ctau_n%5Cwedge+t%7D-X_%7B%5Ctau_%7Bn-1%7D%5Cwedge+t%7D%29%28Y_%7B%5Ctau_n%5Cwedge+t%7D-Y_%7B%5Ctau_%7Bn-1%7D%5Cwedge+t%7D%29%5Csmallskip%5C%5C+%26%5Cdisplaystyle%3D%5Cint_0%5Et%5Cxi%5C%2Cd%5BX%2CY%5D%5EP.+%5Cend%7Barray%7D+&bg=ffffff&fg=000000&s=0&c=20201002) |

Taking the limit of such partitions gives (6).

Now, let ![{\xi\in L^1(X)\cap L^1([X,Y])}](https://s0.wp.com/latex.php?latex=%7B%5Cxi%5Cin+L%5E1%28X%29%5Ccap+L%5E1%28%5BX%2CY%5D%29%7D&bg=ffffff&fg=000000&s=0&c=20201002)

Let ![{\xi\in L^1([X,Y])}](https://s0.wp.com/latex.php?latex=%7B%5Cxi%5Cin+L%5E1%28%5BX%2CY%5D%29%7D&bg=ffffff&fg=000000&s=0&c=20201002)

![\displaystyle \int\xi^n\,d[X,Y]=[Z^n,Y] =Z^nY - \int_0^tY_-\xi^n\,dX-\int Z^n_-\,dY.](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%5Cint%5Cxi%5En%5C%2Cd%5BX%2CY%5D%3D%5BZ%5En%2CY%5D+%3DZ%5EnY+-+%5Cint_0%5EtY_-%5Cxi%5En%5C%2CdX-%5Cint+Z%5En_-%5C%2CdY.+&bg=ffffff&fg=000000&s=0&c=20201002) |

(8) |

By the dominated convergence theorem, the first two terms on the right converge ucp to the limit with

![\displaystyle \int\xi^n\,d[X,Y] \xrightarrow{ucp} ZY-\int_0^t Y_-\xi\,dX-\int Z_-\,dY = \left[\int\xi\,dX,Y\right].](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%5Cint%5Cxi%5En%5C%2Cd%5BX%2CY%5D+%5Cxrightarrow%7Bucp%7D+ZY-%5Cint_0%5Et+Y_-%5Cxi%5C%2CdX-%5Cint+Z_-%5C%2CdY+%3D+%5Cleft%5B%5Cint%5Cxi%5C%2CdX%2CY%5Cright%5D.+&bg=ffffff&fg=000000&s=0&c=20201002) |

(9) |

In particular, if

Next, suppose that

![{\int\xi^n\,d[X,Y]\rightarrow 0}](https://s0.wp.com/latex.php?latex=%7B%5Cint%5Cxi%5En%5C%2Cd%5BX%2CY%5D%5Crightarrow+0%7D&bg=ffffff&fg=000000&s=0&c=20201002)

![{L^1(X)\subseteq L^1([X,Y])}](https://s0.wp.com/latex.php?latex=%7BL%5E1%28X%29%5Csubseteq+L%5E1%28%5BX%2CY%5D%29%7D&bg=ffffff&fg=000000&s=0&c=20201002)

Any

![{\int\xi\,d[X,Y]}](https://s0.wp.com/latex.php?latex=%7B%5Cint%5Cxi%5C%2Cd%5BX%2CY%5D%7D&bg=ffffff&fg=000000&s=0&c=20201002)

So far, we have shown that every

Setting ![{[X,Z]}](https://s0.wp.com/latex.php?latex=%7B%5BX%2CZ%5D%7D&bg=ffffff&fg=000000&s=0&c=20201002)

![{[Z]=\int\xi\,d[X,Z]}](https://s0.wp.com/latex.php?latex=%7B%5BZ%5D%3D%5Cint%5Cxi%5C%2Cd%5BX%2CZ%5D%7D&bg=ffffff&fg=000000&s=0&c=20201002)

![{[X,Z]=\int\xi\,d[X]}](https://s0.wp.com/latex.php?latex=%7B%5BX%2CZ%5D%3D%5Cint%5Cxi%5C%2Cd%5BX%5D%7D&bg=ffffff&fg=000000&s=0&c=20201002)

![\displaystyle \int_0^t\xi^2\,d[X]=\int_0^t\xi\,d[X,Z]=[Z]_t<\infty.](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%5Cint_0%5Et%5Cxi%5E2%5C%2Cd%5BX%5D%3D%5Cint_0%5Et%5Cxi%5C%2Cd%5BX%2CZ%5D%3D%5BZ%5D_t%3C%5Cinfty.+&bg=ffffff&fg=000000&s=0&c=20201002) |

Finally, equation (5) follows from the Kunita-Watanabe inequality,

![\displaystyle \int_0^t\vert\xi\vert\,\vert d[X,Y]\vert\le\sqrt{\int_0^t\xi^2\,d[X]_t\, [Y]_t}<\infty.](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%5Cint_0%5Et%5Cvert%5Cxi%5Cvert%5C%2C%5Cvert+d%5BX%2CY%5D%5Cvert%5Cle%5Csqrt%7B%5Cint_0%5Et%5Cxi%5E2%5C%2Cd%5BX%5D_t%5C%2C+%5BY%5D_t%7D%3C%5Cinfty.+&bg=ffffff&fg=000000&s=0&c=20201002) |

⬜

A simple consequence of Theorem 7 is that stopping the covariation of two semimartingales at a stopping time is the same as stopping either of the individual processes.

Corollary 8 If

is a stopping time then,

In particular,

.

![\displaystyle [X,Y]^\tau = \left[X^\tau,Y\right] = \left[ X, Y^\tau\right].](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%5BX%2CY%5D%5E%5Ctau+%3D+%5Cleft%5BX%5E%5Ctau%2CY%5Cright%5D+%3D+%5Cleft%5B+X%2C+Y%5E%5Ctau%5Cright%5D.+&bg=ffffff&fg=000000&s=0&c=20201002)

Proof: The result follows by integrating ![{1_{(0,\tau]}}](https://s0.wp.com/latex.php?latex=%7B1_%7B%280%2C%5Ctau%5D%7D%7D&bg=ffffff&fg=000000&s=0&c=20201002)

![\displaystyle [X,Y]^\tau=\int 1_{(0,\tau]}\,d[X,Y] = \left[\int 1_{(0,\tau]}\,dX,Y\right]=[X^\tau,Y].](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%5BX%2CY%5D%5E%5Ctau%3D%5Cint+1_%7B%280%2C%5Ctau%5D%7D%5C%2Cd%5BX%2CY%5D+%3D+%5Cleft%5B%5Cint+1_%7B%280%2C%5Ctau%5D%7D%5C%2CdX%2CY%5Cright%5D%3D%5BX%5E%5Ctau%2CY%5D.+&bg=ffffff&fg=000000&s=0&c=20201002) |

⬜

A semimartingale which is small in absolute value does not necessarily have a small quadratic variation or, to state this another way, quadratic variation is not a continuous map under ucp convergence. For example, consider solutions to the stochastic differential equation

![{[X]_t=t}](https://s0.wp.com/latex.php?latex=%7B%5BX%5D_t%3Dt%7D&bg=ffffff&fg=000000&s=0&c=20201002)

Lemma 9 Quadratic covariation defines a jointly continuous map

under the semimartingale topology.

That is, if

,

, X, Y are semimartingales with

, then

and, furthermore, the variation of

on any bounded interval tends to zero in probability.

![\displaystyle \setlength\arraycolsep{2pt} \begin{array}{rl} &\displaystyle \mathcal{S}\times\mathcal{S}\rightarrow\mathcal{S},\smallskip\\ &\displaystyle (X,Y)\mapsto[X,Y] \end{array}](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%5Csetlength%5Carraycolsep%7B2pt%7D+%5Cbegin%7Barray%7D%7Brl%7D+%26%5Cdisplaystyle+%5Cmathcal%7BS%7D%5Ctimes%5Cmathcal%7BS%7D%5Crightarrow%5Cmathcal%7BS%7D%2C%5Csmallskip%5C%5C+%26%5Cdisplaystyle+%28X%2CY%29%5Cmapsto%5BX%2CY%5D+%5Cend%7Barray%7D+&bg=ffffff&fg=000000&s=0&c=20201002)

Proof: We start by showing that if

![{[X^n]_t\rightarrow0}](https://s0.wp.com/latex.php?latex=%7B%5BX%5En%5D_t%5Crightarrow0%7D&bg=ffffff&fg=000000&s=0&c=20201002)

|

tend to infinity in probability. So, it is enough to show that ![{[X^n]_{\tau_n\wedge t}}](https://s0.wp.com/latex.php?latex=%7B%5BX%5En%5D_%7B%5Ctau_n%5Cwedge+t%7D%7D&bg=ffffff&fg=000000&s=0&c=20201002)

![\displaystyle [X^n]_{\tau_n\wedge t}=(X^n_{\tau_n\wedge t})^2-(X^n_0)^2-2\int_0^t1_{(0,\tau_n]}X^n_-\,dX^n.](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%5BX%5En%5D_%7B%5Ctau_n%5Cwedge+t%7D%3D%28X%5En_%7B%5Ctau_n%5Cwedge+t%7D%29%5E2-%28X%5En_0%29%5E2-2%5Cint_0%5Et1_%7B%280%2C%5Ctau_n%5D%7DX%5En_-%5C%2CdX%5En.+&bg=ffffff&fg=000000&s=0&c=20201002) |

The first two terms on the right hand side tend to zero in probability, by ucp convergence. For the final term, for any fixed n, note that ![{1_{(0,\tau_n]}X^n_-}](https://s0.wp.com/latex.php?latex=%7B1_%7B%280%2C%5Ctau_n%5D%7DX%5En_-%7D&bg=ffffff&fg=000000&s=0&c=20201002)

![{{\mathbb E}[\vert\xi_0X_0+\int_0^t\xi\,dX\vert\wedge1]}](https://s0.wp.com/latex.php?latex=%7B%7B%5Cmathbb+E%7D%5B%5Cvert%5Cxi_0X_0%2B%5Cint_0%5Et%5Cxi%5C%2CdX%5Cvert%5Cwedge1%5D%7D&bg=ffffff&fg=000000&s=0&c=20201002)

![\displaystyle \setlength\arraycolsep{2pt} \begin{array}{rl} \displaystyle{\mathbb E}\left[\left\vert\int_0^t1_{(0,\tau_n]}X^n_-\,dX^n\right\vert\wedge1\right]&\displaystyle=\lim_{m\rightarrow\infty}{\mathbb E}\left[\left\vert\int_0^t\xi^m\,dX^n\right\vert\wedge1\right]\smallskip\\&\displaystyle\le D^{\rm sm}_t(X^n). \end{array}](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%5Csetlength%5Carraycolsep%7B2pt%7D+%5Cbegin%7Barray%7D%7Brl%7D+%5Cdisplaystyle%7B%5Cmathbb+E%7D%5Cleft%5B%5Cleft%5Cvert%5Cint_0%5Et1_%7B%280%2C%5Ctau_n%5D%7DX%5En_-%5C%2CdX%5En%5Cright%5Cvert%5Cwedge1%5Cright%5D%26%5Cdisplaystyle%3D%5Clim_%7Bm%5Crightarrow%5Cinfty%7D%7B%5Cmathbb+E%7D%5Cleft%5B%5Cleft%5Cvert%5Cint_0%5Et%5Cxi%5Em%5C%2CdX%5En%5Cright%5Cvert%5Cwedge1%5Cright%5D%5Csmallskip%5C%5C%26%5Cdisplaystyle%5Cle+D%5E%7B%5Crm+sm%7D_t%28X%5En%29.+%5Cend%7Barray%7D+&bg=ffffff&fg=000000&s=0&c=20201002) |

Here, bounded convergence has been used to write the integral as a limit of integrals over

![{\int_0^t1_{(0,\tau_n]}X^n_-\,dX^n}](https://s0.wp.com/latex.php?latex=%7B%5Cint_0%5Et1_%7B%280%2C%5Ctau_n%5D%7DX%5En_-%5C%2CdX%5En%7D&bg=ffffff&fg=000000&s=0&c=20201002)

Now suppose that

![\displaystyle [X^n,Y^n]-[X,Y]=[X^n-X,Y^n-Y]+[X^n-X,Y]+[X,Y^n-Y].](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%5BX%5En%2CY%5En%5D-%5BX%2CY%5D%3D%5BX%5En-X%2CY%5En-Y%5D%2B%5BX%5En-X%2CY%5D%2B%5BX%2CY%5En-Y%5D.+&bg=ffffff&fg=000000&s=0&c=20201002) |

Applying the Kunita-Watanabe inequality (Theorem 6) to each of the three terms on the right hand side shows that this has variation bounded by

![\displaystyle \sqrt{[X^n-X]_t[Y^n-Y]_t}+\sqrt{[X^n-X]_t[Y]_t}+\sqrt{[X]_t[Y^n-Y]_t}](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%5Csqrt%7B%5BX%5En-X%5D_t%5BY%5En-Y%5D_t%7D%2B%5Csqrt%7B%5BX%5En-X%5D_t%5BY%5D_t%7D%2B%5Csqrt%7B%5BX%5D_t%5BY%5En-Y%5D_t%7D+&bg=ffffff&fg=000000&s=0&c=20201002) |

on an interval

Finally, letting

![\displaystyle \setlength\arraycolsep{2pt} \begin{array}{rl} \displaystyle\left\vert\int_0^t\xi^n\,d[X^n,Y^n]-\int_0^t\xi^n\,d[X,Y]\right\vert&\displaystyle\le\int_0^t\vert\xi^n\vert\,dV^n\smallskip\\&\displaystyle\le V^n_t\rightarrow 0 \end{array}](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%5Csetlength%5Carraycolsep%7B2pt%7D+%5Cbegin%7Barray%7D%7Brl%7D+%5Cdisplaystyle%5Cleft%5Cvert%5Cint_0%5Et%5Cxi%5En%5C%2Cd%5BX%5En%2CY%5En%5D-%5Cint_0%5Et%5Cxi%5En%5C%2Cd%5BX%2CY%5D%5Cright%5Cvert%26%5Cdisplaystyle%5Cle%5Cint_0%5Et%5Cvert%5Cxi%5En%5Cvert%5C%2CdV%5En%5Csmallskip%5C%5C%26%5Cdisplaystyle%5Cle+V%5En_t%5Crightarrow+0+%5Cend%7Barray%7D+&bg=ffffff&fg=000000&s=0&c=20201002) |

in probability as n tends to infinity. So ![{[X^n,Y^n]}](https://s0.wp.com/latex.php?latex=%7B%5BX%5En%2CY%5En%5D%7D&bg=ffffff&fg=000000&s=0&c=20201002)

Dear George,

I’m trying to prove a certain type of continuity of the quadratic variation for a fixed time T: for all \epsilon > 0, there exists \delta > 0 such that \|X\|_{+\infty} < \delta \Rightarrow [X]_T < \epsilon. Here \|X\|_{+\infty} = sup_{0 \leq t \leq T} |X_t|. Both inequalities should hold almost surely and X is just a bounded cadlag process in [0,T]. Do you know any reference for this? I've looked for it on a lot of books (Protter, Karatzas and Shreve,…), but I couldn't find anything.

Thank you very much and congratulation, the site is really awesome!

Yuri – There is no such relation between the maximum of a process and its quadratic variation. Actually, X can remain as close to zero as you like at the same time as its quadratic variation being as large as you like. I’ll post an example when I have time to log on.

Start with Brownian motion and make then it jump to zero every time |B_t|=delta > 0. It picks up q-variation at dt + jumps and is uniformly bounded by delta.

Gerard – Yes, that works. I was thinking of something like an Ornstein-Uhlenbeck process with high mean reversion rate. Or f(Wt) for a standard Brownian motion W and f an arbitrarily small function with non-vanishing derivative. Something like f(x) = asin(a−1x) will do.

Hi Gerard and George, I have just seen your examples. Thank you very much, they were really helpful. Best.

I don’t think I understand exactly what Lemma 5 is about. So to move it in a easier case if I have Z=(X,Y) semimartingale – so X,Y semimartingales – and M bounded measurable process I have that![\int M d[X,Y]](https://s0.wp.com/latex.php?latex=%5Cint+M+d%5BX%2CY%5D&bg=ffffff&fg=000000&s=0&c=20201002) is an increasing process?

is an increasing process?

I image that “increasing” here means with respect to the partial ordering on symmetric matrices, not that the individual components are increasing.

soumik – Yes, I am referring to the matrix rather than the individual components (as I mention above the statement of the Lemma). The summation convention is being used in equation (3), so in the case of a pair of semimartingales X, Y it actually means that

is increasing for bounded measurable processes M, N.

Update: I have added an additional result to this post, Lemma 9, showing that quadratic variations and covariations are continuous under the semimartingale topology.

This also relates to Yuri’s question in the comment above. Although a semimartingale which is small in absolute value need not have a small quadratic variation, it is true that a semimartingale which is close to zero in the semimartingale topology has a small quadratic variation (in probability).

Hello,

Thank you for all your posts.

For Lemma 9, is there an equivalent result for Skhorokhod topology instead of semimartingale topology?

Hi. No, I don’t think that there is much you can say here for the Skorokhod topology. Note that the Skorokhod topology is weaker than uniform convergence, so any of the examples given by me and Gerard above are also examples of processes whose paths tend to zero under the Skorokhod topology, but whose quadratic variation does not go to zero.

Dear George,

I’m wondering whether you have posted anywhere about the convergence of the quadratic covariation.

Say $X_n$ and $Y_n$ respectively converge to semimartingales $X$ and $Y$. It would be interesting to know what kind of convergence you would need to impose on $X_n$ and $Y_n$ for their to get convergence of the covariations to the covariation of the limiting semimartingales.

Great post once again!

Sorry, but no I haven’t looked at this beyond Lemma 9 above. Convergence in the semimartingale topology is sufficient. You could, no doubt, come up with weaker conditions which are still sufficent and relevant to whatever specific problems you are looking at. However, I don’t think that the other common kinds of convergence weaker than semimartingale convergence are sufficient on their own.

Thank you for this tremendous work you put in to make these easy to read note available online.

I have two questions though.

1- after equation 2 when you said ” of order….” its in the mean sqare sense right?

2- does the use random partition lead to a largely different quadratic variation concept compared to what we get when using deterministic partition ?

Thanks in advance

Your proof of the Kunita-Watanabe Inequality resembles that of the Cauchy-Schwarz inequality. I was wondering whether one could argue more directly: On the space of measurable processes paired with semimartingales define the inner product

of measurable processes paired with semimartingales define the inner product ![= \int_0^t \alpha_s\beta_s d[X, Y]_s](https://s0.wp.com/latex.php?latex=%3D+%5Cint_0%5Et+%5Calpha_s%5Cbeta_s+d%5BX%2C+Y%5D_s&bg=ffffff&fg=000000&s=0&c=20201002) . Denote by

. Denote by  the random (

the random ( -by-

-by- ) Hahn decomposition of

) Hahn decomposition of ![d[X, Y]](https://s0.wp.com/latex.php?latex=d%5BX%2C+Y%5D&bg=ffffff&fg=000000&s=0&c=20201002) . Conclude by applying C-S to

. Conclude by applying C-S to ![([\mathbf{1}(P) - \mathbf{1}(N)]|\alpha|, X), (|\beta|, Y)](https://s0.wp.com/latex.php?latex=%28%5B%5Cmathbf%7B1%7D%28P%29+-+%5Cmathbf%7B1%7D%28N%29%5D%7C%5Calpha%7C%2C+X%29%2C+%28%7C%5Cbeta%7C%2C+Y%29&bg=ffffff&fg=000000&s=0&c=20201002) .

.

I also meant to say thanks for the excellent blog!

How do i have to interpret the sum in Corollary 2? Is it possible for a semimartingale to have infinitely many jumps in the interval![[0,t]](https://s0.wp.com/latex.php?latex=%5B0%2Ct%5D&bg=ffffff&fg=000000&s=0&c=20201002) ?

?

Hi. No, it can be an infinite sum. There will be only countably many jumps but, generally, infinite sums of non-negative numbers are well-defined.

Hi, thank you for your answer. So the countability is because![[X,X]](https://s0.wp.com/latex.php?latex=%5BX%2CX%5D&bg=ffffff&fg=000000&s=0&c=20201002) is a càdlàg process and therefore we have only countably many s s.t. the jump process of

is a càdlàg process and therefore we have only countably many s s.t. the jump process of ![[X,X]](https://s0.wp.com/latex.php?latex=%5BX%2CX%5D&bg=ffffff&fg=000000&s=0&c=20201002) at time s is greater 1/n for each n (which was proven here: http://math.stackexchange.com/q/1914422/337225). Therefore there are only countably many s s.t. the jump process is greater than zero, since the countable union of countably many jumps is again countable. Is that correct?

at time s is greater 1/n for each n (which was proven here: http://math.stackexchange.com/q/1914422/337225). Therefore there are only countably many s s.t. the jump process is greater than zero, since the countable union of countably many jumps is again countable. Is that correct?

Correct, although maybe it is a bit more direct to use the fact that X is cadlag rather than [X].

On the right side of your formula in the proof of lemma 1, there are probably two “dots” missing for the integration. Because i read

![\Delta XY = X_{-}\Delta Y + Y_{-}\Delta X + \Delta [X,Y]](https://s0.wp.com/latex.php?latex=%5CDelta+XY+%3D+X_%7B-%7D%5CDelta+Y+%2B+Y_%7B-%7D%5CDelta+X+%2B+%5CDelta+%5BX%2CY%5D+&bg=ffffff&fg=000000&s=0&c=20201002) as normal multiplication. Applying the lemma

as normal multiplication. Applying the lemma  gives the desired equality.

gives the desired equality.

I did mean this as normal multiplication, and I don’t quite follow what you mean by .

.

The integration by parts formula tells us that![XY = X_{0}Y_{0}+X_{-}*Y + Y_{-}*X + [X,Y]](https://s0.wp.com/latex.php?latex=XY+%3D+X_%7B0%7DY_%7B0%7D%2BX_%7B-%7D%2AY+%2B+Y_%7B-%7D%2AX+%2B+%5BX%2CY%5D&bg=ffffff&fg=000000&s=0&c=20201002) . Assuming

. Assuming  or

or  , we have

, we have ![XY =X_{-}*Y + Y_{-}*X + [X,Y]](https://s0.wp.com/latex.php?latex=XY+%3DX_%7B-%7D%2AY+%2B+Y_%7B-%7D%2AX+%2B+%5BX%2CY%5D&bg=ffffff&fg=000000&s=0&c=20201002) and thus

and thus ![\Delta(XY) =\Delta(X_{-}*Y) + \Delta(Y_{-}*X) + \Delta[X,Y]](https://s0.wp.com/latex.php?latex=%5CDelta%28XY%29+%3D%5CDelta%28X_%7B-%7D%2AY%29+%2B+%5CDelta%28Y_%7B-%7D%2AX%29+%2B+%5CDelta%5BX%2CY%5D&bg=ffffff&fg=000000&s=0&c=20201002) . But now you probably apply

. But now you probably apply  (that was actually wrong in my first comment), which is only available for locally bounded predictable processes. But i guess

(that was actually wrong in my first comment), which is only available for locally bounded predictable processes. But i guess  and

and  are locally bounded and predictable.

are locally bounded and predictable.

I did indeed apply that result. Corollary 8 from the post on properties of stochastic integral. Actually, locally bounded is not required, just Y-integrability. We do have local boundedness here though, which is how we can be sure that is Y integrable in the first place.

is Y integrable in the first place.

Dear George,

In the proof of equation (8) of Theorem 7 you mention that the sequence in the final term on the right hand side is dominated but you don’t mention which is the dominator. I suppose you can claim that

in the final term on the right hand side is dominated but you don’t mention which is the dominator. I suppose you can claim that  is caglad and proceed.

is caglad and proceed.

Yes, the fact that it converges uniformly guarantees that the supremum is finite, and caglad.

Dear George,

In the statement of Theorem 6 you mention the measure![|d[X,Y]|](https://s0.wp.com/latex.php?latex=%7Cd%5BX%2CY%5D%7C&bg=ffffff&fg=000000&s=0&c=20201002) but you didn’t defined it first. Can you please explain what you mean by that notation ?

but you didn’t defined it first. Can you please explain what you mean by that notation ?

If V is a finite variation process, then I use |dV| for the integral with respect to the variation of V. I use this notation throughout my notes.

Dear George,

I see, well then can you please explain (or give a reference) why the variation of the third term equals the integral of the absolute value with respect to the variation of [X,Y], because I couldn’t find a reference for this result.

I used the result that, for a bounded variation function f, then the variation of is equal to

is equal to  . I did not include a proof, as it is basic (non-stochastic) calculus.

. I did not include a proof, as it is basic (non-stochastic) calculus.

The Hahn decomposition theorem says that where

where  is measurable with absolute value 1. Then,

is measurable with absolute value 1. Then,  for some measurable function

for some measurable function  of absolute value 1. The result follows from this…

of absolute value 1. The result follows from this…

Hi George, how can we prove that the quadratic covariation of a d-dimensional semimartingale is positive semidefinite?

I think I proved that above with the formula

Hello George,

Thank you so much for your posts. For Lemma 3, is the integral the Lebesgue-Stieltjes integral instead of the stochastic integral?

Yes it is. I did mention the Lebesgue-Stieltjes integral in the text just above the statement of the Lemma, but maybe I could have been more explicit that this is what is meant in the statement