In this post I look at the integral Xt = ∫0t 1{W≥0} dW for standard Brownian motion W. This is a particularly interesting example of stochastic integration with connections to local times, option pricing and hedging, and demonstrates behaviour not seen for deterministic integrals that can seem counter-intuitive. For a start, X is a martingale so has zero expectation. To some it might, at first, seem that X is nonnegative and — furthermore — equals W ∨ 0. However, this has positive expectation contradicting the first property. In fact, X can go negative and we can compute its distribution. In a Twitter post, Oswin So asked about this very point, showing some plots demonstrating the behaviour of the integral.

We can evaluate the integral as Xt = Wt ∨ 0 – 12 Lt0 where Lt0 is the local time of W at 0. The local time is a continuous increasing process starting from 0, and only increases at times where W = 0. That is, it is constant over intervals on which W is nonzero. The first term, Wt ∨ 0 has probability density p(x) equal to that of a normal density over x > 0 and has a delta function at zero. Subtracting the nonnegative value L0t spreads out the density of this delta function to the left, leading to the odd looking density computed numerically in So’s Twitter post, with a peak just to the left of the origin and dropping instantly to a smaller value on the right. We will compute an exact form for this probability density but, first, let’s look at an intuitive interpretation in the language of option pricing.

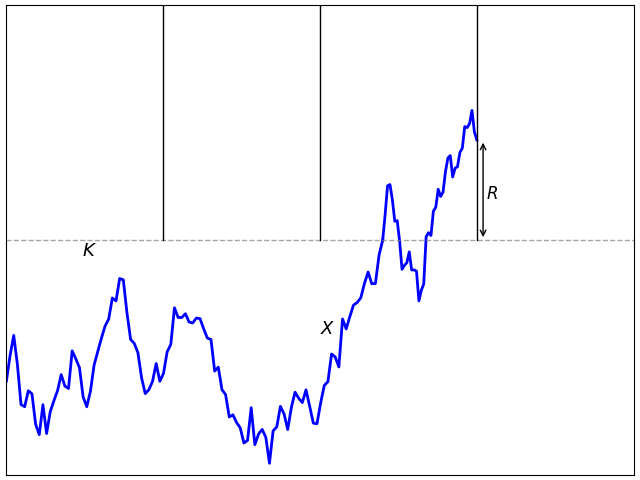

Consider a financial asset such as a stock, whose spot price at time t is St. We suppose that the price is defined at all times t ≥ 0 and has continuous sample paths. Furthermore, suppose that we can buy and sell at spot any time with no transaction costs. A call option of strike price K and maturity T pays out the cash value (ST - K)+ at time T. For simplicity, assume that this is ‘out of the money’ at the initial time, meaning that S0 ≤ K.

The idea of option hedging is, starting with an initial investment, to trade in the stock in such a way that at maturity T, the value of our trading portfolio is equal to (ST - K)+. This synthetically replicates the option. A naive suggestion which is sometimes considered is to hold one unit of stock at all times t for which St ≥ K and zero units at all other times.The profit from such a strategy is given by the integral XT = ∫0T 1{S≥K} dS. If the stock only equals the strike price at finitely many times then this works. If it first hits K at time s and does not drop back below it on interval (s, t) then the profit at t is equal to the amount St – K that it has gone up since we purchased it. If it drops back below the strike then we sell at K for zero profit or loss, and this repeats for subsequent times that it exceeds K. So, at time T, we hold one unit of stock if its value is above K for a profit of ST – K and zero units for zero profit otherwise. This replicates the option payoff.

The idea described works if ST hits the strike K at a finite set of times,and also if the path of St has finite variation, in which case Lebesgue-Stieltjes integration gives XT = (ST - K)+. It cannot work for stock prices though! If it did, then we have a trading strategy which is guaranteed to never lose money but generates profits on the positive probability event that ST > K. This is arbitrage, generating money with zero risk, which should be impossible.

What goes wrong? First, Brownian motion does not have sample paths with finite variation and will not hit a level finitely often. Instead, if it reaches K then it hits the level uncountably often. As our simple trading strategy would involve buying and selling infinitely often, it is not so easy. Instead, we can approximate by a discrete-time strategy and take the limit. Choosing a finite sequence of times 0 = t0 < t1 < ⋯< tn = T, the discrete approximation is to hold one unit of the asset over the interval (ti, ti+1] if Sti ≥ K and zero units otherwise.

The discrete strategy involves buying one unit of the asset whenever its price reaches K at one of the discrete times and selling whenever it drops back below. This replicates the option payoff, except for the fact then when we buy above K we effectively overpay by amount Sti – K and, when we sell below K, we lose K – Sti. This results in some slippage from not being able to execute at the exact level,

|

So, our simple trading strategy generates profit (ST - K)+ – AT, missing the option value by amount AT. In the limit as n goes to infinity with time step size going to zero, the slippage AT does not go to zero. For equally spaced times, It can be shown that the number of times that spot crosses K is of order √n, and each of these times generates slippage of order 1/√n on average. So, in the limit, AT does not vanish and, instead, converges on a positive value equal to half the local time LTK.

Figure 2 shows the situation, with the slippage A shown on the same plot (using K as the zero axis, so they are on the same scale). We can just take K = 0 for an asset whose spot price can be positive or negative. Then, with S = W, our integral XT = ∫0T 1{W≥0} dW is the same as the payoff from the naive option hedge, or (ST)+ minus slippage L0T/2.

Now lets turn to a computation of the probability density of XT = WT ∨ 0 – LT0/2. By the scaling property of Brownian motion, the distribution of XT/√T does not depend on T, so we take T = 1 without loss of generality. The first trick to this is to make use of the fact that, if Mt = sups≤tWs is the running maximum then (|Wt|, Lt0) has the same joint distribution as (Mt - Wt, Mt). This immediately tells us that L10 has the same distribution as M1 which, by the reflection principle, has the same distribution as |W1|. Using

|

for the standard normal density, this shows that the local time L10 has probability density 2φ(x) over x > 0.

Next, as flipping the sign W does not impact either |W1| or L10, sgn(W1) is independent of these. On the event W1 < 0 we have X1 = –L10/2 which has density 4φ(2x) over x < 0. On the event W1 > 0, we have X1 = |W1|-L10/2, which has the same distribution as M1/2 – W1.

To complete the computation of the probability density of X1, we need to know the joint distribution of M1 and W1, which can be done as described in the post on the reflection principle. The probability that W1 is in an interval of width δx about a point x and that M1 > y, for some y > x is, by reflection, equal to the probability that W1 is in an interval of width δx about the point 2y – x. This has probability φ(2y - x)δx and, by differentiating in y, gives a joint probability density of 2φ′(x - 2y) for (W1, M1).

The expectation of f(X1) for bounded measurable function f can be computed by integrating over this joint probability density.

![\displaystyle \begin{aligned} {\mathbb E}[f(X_1)\vert\;W_1 > 0] &={\mathbb E}[f(M_1/2-W_1)]\\ &=2\int_{-\infty}^\infty\int_{x_+}^\infty f(y/2-x)\varphi'(x-2y)\,dydx\\ &=4\int_{-\infty}^\infty\int_{(-x)\vee(-x/2)}^\infty f(z)\varphi'(-3x-4z)\,dzdx\\ &=4\int_{-\infty}^\infty\int_{(-z)\vee(-2z)}^\infty f(z)\varphi'(-3x-4z)\,dxdz\\ &=\frac43\int_{-\infty}^\infty f(z)\varphi(2z)\,dz+\frac43\int_0^\infty f(z)\varphi(z)\,dz. \end{aligned}](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle+%5Cbegin%7Baligned%7D+%7B%5Cmathbb+E%7D%5Bf%28X_1%29%5Cvert%5C%3BW_1+%3E+0%5D+%26%3D%7B%5Cmathbb+E%7D%5Bf%28M_1%2F2-W_1%29%5D%5C%5C+%26%3D2%5Cint_%7B-%5Cinfty%7D%5E%5Cinfty%5Cint_%7Bx_%2B%7D%5E%5Cinfty+f%28y%2F2-x%29%5Cvarphi%27%28x-2y%29%5C%2Cdydx%5C%5C+%26%3D4%5Cint_%7B-%5Cinfty%7D%5E%5Cinfty%5Cint_%7B%28-x%29%5Cvee%28-x%2F2%29%7D%5E%5Cinfty+f%28z%29%5Cvarphi%27%28-3x-4z%29%5C%2Cdzdx%5C%5C+%26%3D4%5Cint_%7B-%5Cinfty%7D%5E%5Cinfty%5Cint_%7B%28-z%29%5Cvee%28-2z%29%7D%5E%5Cinfty+f%28z%29%5Cvarphi%27%28-3x-4z%29%5C%2Cdxdz%5C%5C+%26%3D%5Cfrac43%5Cint_%7B-%5Cinfty%7D%5E%5Cinfty+f%28z%29%5Cvarphi%282z%29%5C%2Cdz%2B%5Cfrac43%5Cint_0%5E%5Cinfty+f%28z%29%5Cvarphi%28z%29%5C%2Cdz.+%5Cend%7Baligned%7D+&bg=ffffff&fg=000000&s=0&c=20201002) |

The substitution z = y/2 – x was applied in the inner integral, and the order of integration switched. The probability density of X1 conditioned on W1 > 0 is therefore,

|

Conditioned on W1 < 0, we have already shown that the density is 4φ(2x) over x < 0 so, taking the average of these, we obtain

|

This is plotted in figure 3 below, agreeing with So’s numerical estimation from the Twitter post shown in figure 1 above.

![\displaystyle V={\mathbb E}\left[f(X_T);\;\sup{}_{t\le T}X_t \ge K\right]](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle+V%3D%7B%5Cmathbb+E%7D%5Cleft%5Bf%28X_T%29%3B%5C%3B%5Csup%7B%7D_%7Bt%5Cle+T%7DX_t+%5Cge+K%5Cright%5D+&bg=ffffff&fg=000000&s=0&c=20201002)

![\displaystyle V={\mathbb E}\left[f(X_T);\;\sup{}_{i=1,\ldots,n}X_{t_i}\ge K\right].](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle+V%3D%7B%5Cmathbb+E%7D%5Cleft%5Bf%28X_T%29%3B%5C%3B%5Csup%7B%7D_%7Bi%3D1%2C%5Cldots%2Cn%7DX_%7Bt_i%7D%5Cge+K%5Cright%5D.+&bg=ffffff&fg=000000&s=0&c=20201002)

![\displaystyle V={\mathbb E}\left[f(X_T);\;\sup{}_{i=1,\ldots,n}M_i\ge K\right].](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle+V%3D%7B%5Cmathbb+E%7D%5Cleft%5Bf%28X_T%29%3B%5C%3B%5Csup%7B%7D_%7Bi%3D1%2C%5Cldots%2Cn%7DM_i%5Cge+K%5Cright%5D.+&bg=ffffff&fg=000000&s=0&c=20201002)

![\displaystyle c_p^{-1}{\mathbb E}[[M]^{p/2}_\tau]\le{\mathbb E}[\bar M_\tau^p]\le C_p{\mathbb E}[[M]^{p/2}_\tau].](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++c_p%5E%7B-1%7D%7B%5Cmathbb+E%7D%5B%5BM%5D%5E%7Bp%2F2%7D_%5Ctau%5D%5Cle%7B%5Cmathbb+E%7D%5B%5Cbar+M_%5Ctau%5Ep%5D%5Cle+C_p%7B%5Cmathbb+E%7D%5B%5BM%5D%5E%7Bp%2F2%7D_%5Ctau%5D.+&bg=ffffff&fg=000000&s=0&c=20201002)

is the running maximum,

is the running maximum, ![{[M]}](https://s0.wp.com/latex.php?latex=%7B%5BM%5D%7D&bg=ffffff&fg=000000&s=0&c=20201002) is the quadratic variation,

is the quadratic variation,  is a

is a  is a real number greater than or equal to 1. Then,

is a real number greater than or equal to 1. Then,  and

and  are positive constants depending on p, but independent of the choice of local martingale and stopping time. Furthermore, for continuous local martingales, which are the focus of this post, the inequality holds for all

are positive constants depending on p, but independent of the choice of local martingale and stopping time. Furthermore, for continuous local martingales, which are the focus of this post, the inequality holds for all  .

.![{[M]_0=M_0^2}](https://s0.wp.com/latex.php?latex=%7B%5BM%5D_0%3DM_0%5E2%7D&bg=ffffff&fg=000000&s=0&c=20201002) . Henceforth, I will assume that this is the case, which means that if we are working with the definition in my notes then we should add

. Henceforth, I will assume that this is the case, which means that if we are working with the definition in my notes then we should add  everywhere to the quadratic variation

everywhere to the quadratic variation ![\displaystyle c_p^{-1}[M]^{p/2}+\int\alpha dM\le\bar M^p\le C_p[M]^{p/2}+\int\beta dM](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++c_p%5E%7B-1%7D%5BM%5D%5E%7Bp%2F2%7D%2B%5Cint%5Calpha+dM%5Cle%5Cbar+M%5Ep%5Cle+C_p%5BM%5D%5E%7Bp%2F2%7D%2B%5Cint%5Cbeta+dM+&bg=ffffff&fg=000000&s=0&c=20201002)

. Inequalities in this form are considerably stronger than (

. Inequalities in this form are considerably stronger than ( for a local (sub)martingale N starting from zero. Then,

for a local (sub)martingale N starting from zero. Then, ![{{\mathbb E}[X_\tau]\le{\mathbb E}[Y_\tau]}](https://s0.wp.com/latex.php?latex=%7B%7B%5Cmathbb+E%7D%5BX_%5Ctau%5D%5Cle%7B%5Cmathbb+E%7D%5BY_%5Ctau%5D%7D&bg=ffffff&fg=000000&s=0&c=20201002) for all stopping times

for all stopping times  be an increasing sequence of bounded stopping times increasing to infinity such that the stopped processes

be an increasing sequence of bounded stopping times increasing to infinity such that the stopped processes  are submartingales. Then,

are submartingales. Then,![\displaystyle {\mathbb E}[1_{\{\tau_n\ge\tau\}}X_\tau]\le{\mathbb E}[X_{\tau_n\wedge\tau}]={\mathbb E}[Y_{\tau_n\wedge\tau}]-{\mathbb E}[N_{\tau_n\wedge\tau}]\le{\mathbb E}[Y_{\tau_n\wedge\tau}]\le{\mathbb E}[Y_\tau].](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%7B%5Cmathbb+E%7D%5B1_%7B%5C%7B%5Ctau_n%5Cge%5Ctau%5C%7D%7DX_%5Ctau%5D%5Cle%7B%5Cmathbb+E%7D%5BX_%7B%5Ctau_n%5Cwedge%5Ctau%7D%5D%3D%7B%5Cmathbb+E%7D%5BY_%7B%5Ctau_n%5Cwedge%5Ctau%7D%5D-%7B%5Cmathbb+E%7D%5BN_%7B%5Ctau_n%5Cwedge%5Ctau%7D%5D%5Cle%7B%5Cmathbb+E%7D%5BY_%7B%5Ctau_n%5Cwedge%5Ctau%7D%5D%5Cle%7B%5Cmathbb+E%7D%5BY_%5Ctau%5D.+&bg=ffffff&fg=000000&s=0&c=20201002)

. As usual, I am using

. As usual, I am using  to represent the maximum of two numbers.

to represent the maximum of two numbers. . For any

. For any  we have,

we have,

and X is increasing then,

and X is increasing then,

to denote the running maximum of a process.

to denote the running maximum of a process.![{{\mathbb P}\left(\bar X_t \ge K\right)\le K^{-1}{\mathbb E}[X_t]}](https://s0.wp.com/latex.php?latex=%7B%7B%5Cmathbb+P%7D%5Cleft%28%5Cbar+X_t+%5Cge+K%5Cright%29%5Cle+K%5E%7B-1%7D%7B%5Cmathbb+E%7D%5BX_t%5D%7D&bg=ffffff&fg=000000&s=0&c=20201002) for all

for all  .

. for all

for all  .

.![{{\mathbb E}[\bar X_t]\le(e/(e-1)){\mathbb E}[X_t\log X_t+1]}](https://s0.wp.com/latex.php?latex=%7B%7B%5Cmathbb+E%7D%5B%5Cbar+X_t%5D%5Cle%28e%2F%28e-1%29%29%7B%5Cmathbb+E%7D%5BX_t%5Clog+X_t%2B1%5D%7D&bg=ffffff&fg=000000&s=0&c=20201002) .

.

![\displaystyle {\mathbb P}(\bar X_t\ge K)\le\inf_{x < K}\frac{{\mathbb E}[(X_t-x)_+]}{K-x}.](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%7B%5Cmathbb+P%7D%28%5Cbar+X_t%5Cge+K%29%5Cle%5Cinf_%7Bx+%3C+K%7D%5Cfrac%7B%7B%5Cmathbb+E%7D%5B%28X_t-x%29_%2B%5D%7D%7BK-x%7D.+&bg=ffffff&fg=000000&s=0&c=20201002)

, there exists a martingale with this terminal distribution for which (

, there exists a martingale with this terminal distribution for which ( in (

in (![\displaystyle {\mathbb E}[F(\bar X_t)]\le{\mathbb E}[G(X_t)]](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%7B%5Cmathbb+E%7D%5BF%28%5Cbar+X_t%29%5D%5Cle%7B%5Cmathbb+E%7D%5BG%28X_t%29%5D+&bg=ffffff&fg=000000&s=0&c=20201002)

. The aim of this post is to show how they have a more general `pathwise’ form,

. The aim of this post is to show how they have a more general `pathwise’ form,

. It is relatively straightforward to show that (

. It is relatively straightforward to show that ( will be of the form

will be of the form  for an increasing right-continuous function

for an increasing right-continuous function  , so

, so

, so can be used as the definition of

, so can be used as the definition of  . In the case where X is a semimartingale, integration by parts ensures that this agrees with the stochastic integral

. In the case where X is a semimartingale, integration by parts ensures that this agrees with the stochastic integral  . Since we now have an interpretation of (

. Since we now have an interpretation of ( to be a cadlag real-valued function. Hence, we reduce the martingale inequalities to straightforward results of real-analysis not requiring any probability theory and, consequently, are much more general. I state the precise pathwise generalizations of Doob’s inequalities now, leaving the proof until later in the post. As the first of inequality of theorem

to be a cadlag real-valued function. Hence, we reduce the martingale inequalities to straightforward results of real-analysis not requiring any probability theory and, consequently, are much more general. I state the precise pathwise generalizations of Doob’s inequalities now, leaving the proof until later in the post. As the first of inequality of theorem  ,

,

.

. then,

then,

.

.

.

. , we denote the projection from

, we denote the projection from  by

by

then, for every

then, for every  , there exists a

, there exists a  such that

such that  . The measurable section theorem says that this choice can be made in a measurable way. That is, using

. The measurable section theorem says that this choice can be made in a measurable way. That is, using  to denote the

to denote the  then

then  and there is a measurable map

and there is a measurable map

by setting

by setting  outside of

outside of  .

.

. The graph of

. The graph of ![\displaystyle [\tau]=\left\{(\omega,\tau(\omega))\colon\tau(\omega)\in{\mathbb R}\right\}\subseteq\Omega\times{\mathbb R}.](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%5B%5Ctau%5D%3D%5Cleft%5C%7B%28%5Comega%2C%5Ctau%28%5Comega%29%29%5Ccolon%5Ctau%28%5Comega%29%5Cin%7B%5Cmathbb+R%7D%5Cright%5C%7D%5Csubseteq%5COmega%5Ctimes%7B%5Cmathbb+R%7D.+&bg=ffffff&fg=000000&s=0&c=20201002)

whenever

whenever  can then be expressed by stating that

can then be expressed by stating that ![{[\tau]\subseteq S}](https://s0.wp.com/latex.php?latex=%7B%5B%5Ctau%5D%5Csubseteq+S%7D&bg=ffffff&fg=000000&s=0&c=20201002) . This also ensures that

. This also ensures that  is a subset of

is a subset of  .

. on a set X denotes, simply, a collection of subsets of X. The pair

on a set X denotes, simply, a collection of subsets of X. The pair  is then referred to as a paved space. Given a pair of paved spaces

is then referred to as a paved space. Given a pair of paved spaces  , the product paving

, the product paving  denotes the collection of cartesian products

denotes the collection of cartesian products  for

for  and

and  , which is a paving on

, which is a paving on  . The notation

. The notation  is used for the collection of countable intersections of a paving

is used for the collection of countable intersections of a paving

. It is not clear that

. It is not clear that  is measurable, and we do not rely on this, although

is measurable, and we do not rely on this, although  be a measurable space,

be a measurable space,  be the collection of compact intervals in

be the collection of compact intervals in  , and

, and  under finite unions.

under finite unions. is measurable and its graph

is measurable and its graph ![{[D(S)]}](https://s0.wp.com/latex.php?latex=%7B%5BD%28S%29%5D%7D&bg=ffffff&fg=000000&s=0&c=20201002) is contained in S.

is contained in S.  . The

. The  , of

, of  consists of the sets

consists of the sets  such that there exists

such that there exists  with

with  and

and  . The probability space is complete if

. The probability space is complete if  . More generally,

. More generally,  on the sigma-algebra

on the sigma-algebra  , where B and C are as above. Then

, where B and C are as above. Then  is the completion of

is the completion of  in

in  , and its measure is referred to as the outer measure of A. For any probability measure

, and its measure is referred to as the outer measure of A. For any probability measure  by approximating

by approximating

. We will be concerned primarily with the outer measure

. We will be concerned primarily with the outer measure  , and will show that that if A is the projection of some

, and will show that that if A is the projection of some  , then A can be approximated from below in the following sense: there exists

, then A can be approximated from below in the following sense: there exists  in

in  . From this, it will follow that A is in the completion of

. From this, it will follow that A is in the completion of  which is increasing, continuous along increasing sequences, and continuous along decreasing sequences in

which is increasing, continuous along increasing sequences, and continuous along decreasing sequences in  then

then  .

. is increasing in n then

is increasing in n then  as

as  .

. is decreasing in n then

is decreasing in n then  as

as  for all

for all  .

. .

. , where

, where  is the projection

is the projection  . Then,

. Then,  . Although it looks like a very basic property of measurable sets, maybe even obvious, measurable projection is a surprisingly difficult result to prove. In fact, the requirement that the probability space is complete is necessary and, if it is dropped, then

. Although it looks like a very basic property of measurable sets, maybe even obvious, measurable projection is a surprisingly difficult result to prove. In fact, the requirement that the probability space is complete is necessary and, if it is dropped, then  need not be measurable. Counterexamples exist for commonly used measurable spaces such as

need not be measurable. Counterexamples exist for commonly used measurable spaces such as  and

and  . This suggests that there is something deeper going on here than basic manipulations of measurable sets.

. This suggests that there is something deeper going on here than basic manipulations of measurable sets. be such that

be such that  is convex in x and right-continuous and decreasing in t. Then, for any

is convex in x and right-continuous and decreasing in t. Then, for any  is a semimartingale.

is a semimartingale.

. In the case where f is twice continuously differentiable then the process V is given by

. In the case where f is twice continuously differentiable then the process V is given by  where

where  and

and  are convex in x and increasing in t.

are convex in x and increasing in t.

-integrable martingale, any

-integrable martingale, any  is enough to guarantee that Y is a martingale. Also, it is a

is enough to guarantee that Y is a martingale. Also, it is a  to denote the running (absolute) maximum of a process X. Then, Doob’s

to denote the running (absolute) maximum of a process X. Then, Doob’s

. Here,

. Here,  denotes the standard

denotes the standard ![{\lVert U\rVert_p\equiv{\mathbb E}[U^p]^{1/p}}](https://s0.wp.com/latex.php?latex=%7B%5ClVert+U%5CrVert_p%5Cequiv%7B%5Cmathbb+E%7D%5BU%5Ep%5D%5E%7B1%2Fp%7D%7D&bg=ffffff&fg=000000&s=0&c=20201002) .

. there exists a strictly positive cadlag

there exists a strictly positive cadlag ![{\{X_t\}_{t\in[0,1]}}](https://s0.wp.com/latex.php?latex=%7B%5C%7BX_t%5C%7D_%7Bt%5Cin%5B0%2C1%5D%7D%7D&bg=ffffff&fg=000000&s=0&c=20201002) with

with  .

.  . So, supposing that (

. So, supposing that ( in place of

in place of  . By choosing

. By choosing  as close to

as close to  and

and