Spitzer’s formula is a remarkable result giving the precise joint distribution of the maximum and terminal value of a random walk in terms of the marginal distributions of the process. I have already covered the use of the reflection principle to describe the maximum of Brownian motion, and the same technique can be used for simple symmetric random walks which have a step size of ±1. What is remarkable about Spitzer’s formula is that it applies to random walks with any step distribution.

We consider partial sums

|

for an independent identically distributed (IID) sequence of real-valued random variables X1, X2, …. This ranges over index n = 0, 1, … starting at S0 = 0 and has running maximum

|

Spitzer’s theorem is typically stated in terms of characteristic functions, giving the distributions of (Rn, Sn) in terms of the distributions of the positive and negative parts, Sn+ and Sn–, of the random walk.

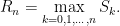

Theorem 1 (Spitzer) For α, β ∈ ℝ,

(1) where ϕn, wn are the characteristic functions

![\displaystyle \begin{aligned} \phi_n(\alpha,\beta)&={\mathbb E}\left[e^{i\alpha R_n+i\beta(R_n-S_n)}\right],\\ w_n(\alpha,\beta)&={\mathbb E}\left[e^{i\alpha S_n^++i\beta S_n^-}\right]\\ &={\mathbb E}\left[e^{i\alpha S_n^+}\right]+{\mathbb E}\left[e^{i\beta S_n^-}\right]-1. \end{aligned}](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle+%5Cbegin%7Baligned%7D+%5Cphi_n%28%5Calpha%2C%5Cbeta%29%26%3D%7B%5Cmathbb+E%7D%5Cleft%5Be%5E%7Bi%5Calpha+R_n%2Bi%5Cbeta%28R_n-S_n%29%7D%5Cright%5D%2C%5C%5C+w_n%28%5Calpha%2C%5Cbeta%29%26%3D%7B%5Cmathbb+E%7D%5Cleft%5Be%5E%7Bi%5Calpha+S_n%5E%2B%2Bi%5Cbeta+S_n%5E-%7D%5Cright%5D%5C%5C+%26%3D%7B%5Cmathbb+E%7D%5Cleft%5Be%5E%7Bi%5Calpha+S_n%5E%2B%7D%5Cright%5D%2B%7B%5Cmathbb+E%7D%5Cleft%5Be%5E%7Bi%5Cbeta+S_n%5E-%7D%5Cright%5D-1.+%5Cend%7Baligned%7D+&bg=ffffff&fg=000000&s=0&c=20201002)

As characteristic functions are bounded by 1, the infinite sums in (1) converge for |t|< 1. However, convergence is not really necessary to interpret this formula, since both sides can be considered as formal power series in indeterminate t, with equality meaning that coefficients of powers of t are equated. Comparing powers of t gives

|

(2) |

and so on.

Spitzer’s theorem in the form above describes the joint distribution of the nonnegative random variables (Rn, Rn - Sn) in terms of the nonnegative variables (Sn+, Sn–). While this does have a nice symmetry, it is often more convenient to look at the distribution of (Rn, Sn) in terms of (Sn+, Sn), which is achieved by replacing α with α + β and β with –β in (1). This gives a slightly different, but equivalent, version of the theorem.

Theorem 2 (Spitzer) For α, β ∈ ℝ,

(3) where ϕ̃n, w̃n are the characteristic functions

![\displaystyle \begin{aligned} \tilde\phi_n(\alpha,\beta)&={\mathbb E}\left[e^{i\alpha R_n+i\beta S_n}\right],\\ \tilde w_n(\alpha,\beta)&={\mathbb E}\left[e^{i\alpha S_n^++i\beta S_n}\right]. \end{aligned}](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle+%5Cbegin%7Baligned%7D+%5Ctilde%5Cphi_n%28%5Calpha%2C%5Cbeta%29%26%3D%7B%5Cmathbb+E%7D%5Cleft%5Be%5E%7Bi%5Calpha+R_n%2Bi%5Cbeta+S_n%7D%5Cright%5D%2C%5C%5C+%5Ctilde+w_n%28%5Calpha%2C%5Cbeta%29%26%3D%7B%5Cmathbb+E%7D%5Cleft%5Be%5E%7Bi%5Calpha+S_n%5E%2B%2Bi%5Cbeta+S_n%7D%5Cright%5D.+%5Cend%7Baligned%7D+&bg=ffffff&fg=000000&s=0&c=20201002)

Taking β = 0 in either (1) or (3) gives the distribution of Rn in terms of Sn+,

![\displaystyle \sum_{n=0}^\infty {\mathbb E}\left[e^{i\alpha R_n}\right]t^n=\exp\left(\sum_{n=1}^\infty {\mathbb E}\left[e^{i\alpha S_n^+}\right]\frac{t^n}n\right)](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle+%5Csum_%7Bn%3D0%7D%5E%5Cinfty+%7B%5Cmathbb+E%7D%5Cleft%5Be%5E%7Bi%5Calpha+R_n%7D%5Cright%5Dt%5En%3D%5Cexp%5Cleft%28%5Csum_%7Bn%3D1%7D%5E%5Cinfty+%7B%5Cmathbb+E%7D%5Cleft%5Be%5E%7Bi%5Calpha+S_n%5E%2B%7D%5Cright%5D%5Cfrac%7Bt%5En%7Dn%5Cright%29+&bg=ffffff&fg=000000&s=0&c=20201002) |

(4) |

I will give a proof of Spitzer’s theorem below. First, though, let’s look at some consequences, starting with the following strikingly simple result for the expected maximum of a random walk.

Corollary 3 For each n ≥ 0,

(5)

![\displaystyle {\mathbb E}[R_n]=\sum_{k=1}^n\frac1k{\mathbb E}[S_k^+].](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle+%7B%5Cmathbb+E%7D%5BR_n%5D%3D%5Csum_%7Bk%3D1%7D%5En%5Cfrac1k%7B%5Cmathbb+E%7D%5BS_k%5E%2B%5D.+&bg=ffffff&fg=000000&s=0&c=20201002)

Proof: As Rn ≥ S1+ = X1+, if Xk+ have infinite mean then both sides of (5) are infinite. On the other hand, if Xk+ have finite mean then so do Sn+ and Rn. Using the fact that the derivative of the characteristic function of an integrable random variable at 0 is just i times its expected value, compute the derivative of (4) at α = 0,

![\displaystyle \begin{aligned} \sum_{n=0}^\infty i{\mathbb E}[R_n]t^n &=\exp\left(\sum_{n=1}^\infty \frac{t^n}n\right)\sum_{n=1}^\infty i{\mathbb E}[S_n^+]\frac{t^n}n\\ &=\exp\left(-\log(1-t)\right)\sum_{n=1}^\infty i{\mathbb E}[S_n^+]\frac{t^n}n\\ &=(1-t)^{-1}\sum_{n=1}^\infty i{\mathbb E}[S_n^+]\frac{t^n}n\\ &=(1+t+t^2+\cdots)\sum_{n=1}^\infty i{\mathbb E}[S_n^+]\frac{t^n}n. \end{aligned}](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle+%5Cbegin%7Baligned%7D+%5Csum_%7Bn%3D0%7D%5E%5Cinfty+i%7B%5Cmathbb+E%7D%5BR_n%5Dt%5En+%26%3D%5Cexp%5Cleft%28%5Csum_%7Bn%3D1%7D%5E%5Cinfty+%5Cfrac%7Bt%5En%7Dn%5Cright%29%5Csum_%7Bn%3D1%7D%5E%5Cinfty+i%7B%5Cmathbb+E%7D%5BS_n%5E%2B%5D%5Cfrac%7Bt%5En%7Dn%5C%5C+%26%3D%5Cexp%5Cleft%28-%5Clog%281-t%29%5Cright%29%5Csum_%7Bn%3D1%7D%5E%5Cinfty+i%7B%5Cmathbb+E%7D%5BS_n%5E%2B%5D%5Cfrac%7Bt%5En%7Dn%5C%5C+%26%3D%281-t%29%5E%7B-1%7D%5Csum_%7Bn%3D1%7D%5E%5Cinfty+i%7B%5Cmathbb+E%7D%5BS_n%5E%2B%5D%5Cfrac%7Bt%5En%7Dn%5C%5C+%26%3D%281%2Bt%2Bt%5E2%2B%5Ccdots%29%5Csum_%7Bn%3D1%7D%5E%5Cinfty+i%7B%5Cmathbb+E%7D%5BS_n%5E%2B%5D%5Cfrac%7Bt%5En%7Dn.+%5Cend%7Baligned%7D+&bg=ffffff&fg=000000&s=0&c=20201002) |

Equating powers of t gives the result. ⬜

The expression for the distribution of Rn in terms of Sn+ might not be entirely intuitive at first glance. Sure, it describes the characteristic functions and, hence, determines the distribution. However, we can describe it more explicitly. As suggested by the evaluation of the first few terms in (2), each ϕn is a convex combination of products of the wn. As is well known, the characteristic function of the sum of random variables is equal to the product of their characteristic functions. Also, if we select a random variable at random from a finite set, then its characteristic function is a convex combination of those of the individual variables with coefficients corresponding to the probabilities in the random choice. So, (3) expresses the distribution of (Rn, Sn) as a random choice of sums of independent copies of (Sk+, Sk).

In fact, expressions such as (1,3) are common in many branches of maths, such as zeta functions associated with curves over finite fields. We have a power series which can be expressed in two different ways,

|

The left hand side is the generating function of the sequence an. The right hand side is a kind of zeta function associated with the sequence bn, and is sometimes referred to as the combinatorial zeta function. The logarithmic derivative gives Σnbntn-1, which is the generating function of bn+1. Continue reading “Spitzer’s Formula”

![\displaystyle \begin{aligned} {\mathbb E}[f(X_1)\vert\;W_1 > 0] &={\mathbb E}[f(M_1/2-W_1)]\\ &=2\int_{-\infty}^\infty\int_{x_+}^\infty f(y/2-x)\varphi'(x-2y)\,dydx\\ &=4\int_{-\infty}^\infty\int_{(-x)\vee(-x/2)}^\infty f(z)\varphi'(-3x-4z)\,dzdx\\ &=4\int_{-\infty}^\infty\int_{(-z)\vee(-2z)}^\infty f(z)\varphi'(-3x-4z)\,dxdz\\ &=\frac43\int_{-\infty}^\infty f(z)\varphi(2z)\,dz+\frac43\int_0^\infty f(z)\varphi(z)\,dz. \end{aligned}](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle+%5Cbegin%7Baligned%7D+%7B%5Cmathbb+E%7D%5Bf%28X_1%29%5Cvert%5C%3BW_1+%3E+0%5D+%26%3D%7B%5Cmathbb+E%7D%5Bf%28M_1%2F2-W_1%29%5D%5C%5C+%26%3D2%5Cint_%7B-%5Cinfty%7D%5E%5Cinfty%5Cint_%7Bx_%2B%7D%5E%5Cinfty+f%28y%2F2-x%29%5Cvarphi%27%28x-2y%29%5C%2Cdydx%5C%5C+%26%3D4%5Cint_%7B-%5Cinfty%7D%5E%5Cinfty%5Cint_%7B%28-x%29%5Cvee%28-x%2F2%29%7D%5E%5Cinfty+f%28z%29%5Cvarphi%27%28-3x-4z%29%5C%2Cdzdx%5C%5C+%26%3D4%5Cint_%7B-%5Cinfty%7D%5E%5Cinfty%5Cint_%7B%28-z%29%5Cvee%28-2z%29%7D%5E%5Cinfty+f%28z%29%5Cvarphi%27%28-3x-4z%29%5C%2Cdxdz%5C%5C+%26%3D%5Cfrac43%5Cint_%7B-%5Cinfty%7D%5E%5Cinfty+f%28z%29%5Cvarphi%282z%29%5C%2Cdz%2B%5Cfrac43%5Cint_0%5E%5Cinfty+f%28z%29%5Cvarphi%28z%29%5C%2Cdz.+%5Cend%7Baligned%7D+&bg=ffffff&fg=000000&s=0&c=20201002)

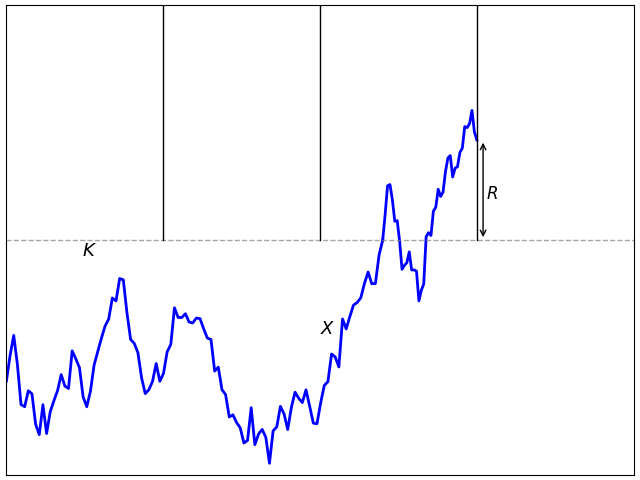

![\displaystyle V={\mathbb E}\left[f(X_T);\;\sup{}_{t\le T}X_t \ge K\right]](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle+V%3D%7B%5Cmathbb+E%7D%5Cleft%5Bf%28X_T%29%3B%5C%3B%5Csup%7B%7D_%7Bt%5Cle+T%7DX_t+%5Cge+K%5Cright%5D+&bg=ffffff&fg=000000&s=0&c=20201002)

![\displaystyle V={\mathbb E}\left[f(X_T);\;\sup{}_{i=1,\ldots,n}X_{t_i}\ge K\right].](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle+V%3D%7B%5Cmathbb+E%7D%5Cleft%5Bf%28X_T%29%3B%5C%3B%5Csup%7B%7D_%7Bi%3D1%2C%5Cldots%2Cn%7DX_%7Bt_i%7D%5Cge+K%5Cright%5D.+&bg=ffffff&fg=000000&s=0&c=20201002)

![\displaystyle V={\mathbb E}\left[f(X_T);\;\sup{}_{i=1,\ldots,n}M_i\ge K\right].](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle+V%3D%7B%5Cmathbb+E%7D%5Cleft%5Bf%28X_T%29%3B%5C%3B%5Csup%7B%7D_%7Bi%3D1%2C%5Cldots%2Cn%7DM_i%5Cge+K%5Cright%5D.+&bg=ffffff&fg=000000&s=0&c=20201002)

![\displaystyle {\mathbb E}[X^s]=2\xi(s),](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%7B%5Cmathbb+E%7D%5BX%5Es%5D%3D2%5Cxi%28s%29%2C+&bg=ffffff&fg=000000&s=0&c=20201002)

![\displaystyle {\mathbb E}[X^s]=\frac{1-2^{1-s}}{s-1}2\xi(s)](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%7B%5Cmathbb+E%7D%5BX%5Es%5D%3D%5Cfrac%7B1-2%5E%7B1-s%7D%7D%7Bs-1%7D2%5Cxi%28s%29+&bg=ffffff&fg=000000&s=0&c=20201002)

![\displaystyle c_p^{-1}{\mathbb E}[[M]^{p/2}_\tau]\le{\mathbb E}[\bar M_\tau^p]\le C_p{\mathbb E}[[M]^{p/2}_\tau].](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++c_p%5E%7B-1%7D%7B%5Cmathbb+E%7D%5B%5BM%5D%5E%7Bp%2F2%7D_%5Ctau%5D%5Cle%7B%5Cmathbb+E%7D%5B%5Cbar+M_%5Ctau%5Ep%5D%5Cle+C_p%7B%5Cmathbb+E%7D%5B%5BM%5D%5E%7Bp%2F2%7D_%5Ctau%5D.+&bg=ffffff&fg=000000&s=0&c=20201002)

is the running maximum,

is the running maximum, ![{[M]}](https://s0.wp.com/latex.php?latex=%7B%5BM%5D%7D&bg=ffffff&fg=000000&s=0&c=20201002) is the quadratic variation,

is the quadratic variation,  is a

is a  is a real number greater than or equal to 1. Then,

is a real number greater than or equal to 1. Then,  and

and  are positive constants depending on p, but independent of the choice of local martingale and stopping time. Furthermore, for continuous local martingales, which are the focus of this post, the inequality holds for all

are positive constants depending on p, but independent of the choice of local martingale and stopping time. Furthermore, for continuous local martingales, which are the focus of this post, the inequality holds for all  .

.![{[M]_0=M_0^2}](https://s0.wp.com/latex.php?latex=%7B%5BM%5D_0%3DM_0%5E2%7D&bg=ffffff&fg=000000&s=0&c=20201002) . Henceforth, I will assume that this is the case, which means that if we are working with the definition in my notes then we should add

. Henceforth, I will assume that this is the case, which means that if we are working with the definition in my notes then we should add  everywhere to the quadratic variation

everywhere to the quadratic variation ![\displaystyle c_p^{-1}[M]^{p/2}+\int\alpha dM\le\bar M^p\le C_p[M]^{p/2}+\int\beta dM](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++c_p%5E%7B-1%7D%5BM%5D%5E%7Bp%2F2%7D%2B%5Cint%5Calpha+dM%5Cle%5Cbar+M%5Ep%5Cle+C_p%5BM%5D%5E%7Bp%2F2%7D%2B%5Cint%5Cbeta+dM+&bg=ffffff&fg=000000&s=0&c=20201002)

. Inequalities in this form are considerably stronger than (

. Inequalities in this form are considerably stronger than ( for a local (sub)martingale N starting from zero. Then,

for a local (sub)martingale N starting from zero. Then, ![{{\mathbb E}[X_\tau]\le{\mathbb E}[Y_\tau]}](https://s0.wp.com/latex.php?latex=%7B%7B%5Cmathbb+E%7D%5BX_%5Ctau%5D%5Cle%7B%5Cmathbb+E%7D%5BY_%5Ctau%5D%7D&bg=ffffff&fg=000000&s=0&c=20201002) for all stopping times

for all stopping times  be an increasing sequence of bounded stopping times increasing to infinity such that the stopped processes

be an increasing sequence of bounded stopping times increasing to infinity such that the stopped processes  are submartingales. Then,

are submartingales. Then,![\displaystyle {\mathbb E}[1_{\{\tau_n\ge\tau\}}X_\tau]\le{\mathbb E}[X_{\tau_n\wedge\tau}]={\mathbb E}[Y_{\tau_n\wedge\tau}]-{\mathbb E}[N_{\tau_n\wedge\tau}]\le{\mathbb E}[Y_{\tau_n\wedge\tau}]\le{\mathbb E}[Y_\tau].](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%7B%5Cmathbb+E%7D%5B1_%7B%5C%7B%5Ctau_n%5Cge%5Ctau%5C%7D%7DX_%5Ctau%5D%5Cle%7B%5Cmathbb+E%7D%5BX_%7B%5Ctau_n%5Cwedge%5Ctau%7D%5D%3D%7B%5Cmathbb+E%7D%5BY_%7B%5Ctau_n%5Cwedge%5Ctau%7D%5D-%7B%5Cmathbb+E%7D%5BN_%7B%5Ctau_n%5Cwedge%5Ctau%7D%5D%5Cle%7B%5Cmathbb+E%7D%5BY_%7B%5Ctau_n%5Cwedge%5Ctau%7D%5D%5Cle%7B%5Cmathbb+E%7D%5BY_%5Ctau%5D.+&bg=ffffff&fg=000000&s=0&c=20201002)

. As usual, I am using

. As usual, I am using  to represent the maximum of two numbers.

to represent the maximum of two numbers. . For any

. For any  we have,

we have,

and X is increasing then,

and X is increasing then,

to denote the running maximum of a process.

to denote the running maximum of a process.![{{\mathbb P}\left(\bar X_t \ge K\right)\le K^{-1}{\mathbb E}[X_t]}](https://s0.wp.com/latex.php?latex=%7B%7B%5Cmathbb+P%7D%5Cleft%28%5Cbar+X_t+%5Cge+K%5Cright%29%5Cle+K%5E%7B-1%7D%7B%5Cmathbb+E%7D%5BX_t%5D%7D&bg=ffffff&fg=000000&s=0&c=20201002) for all

for all  .

. for all

for all  .

.![{{\mathbb E}[\bar X_t]\le(e/(e-1)){\mathbb E}[X_t\log X_t+1]}](https://s0.wp.com/latex.php?latex=%7B%7B%5Cmathbb+E%7D%5B%5Cbar+X_t%5D%5Cle%28e%2F%28e-1%29%29%7B%5Cmathbb+E%7D%5BX_t%5Clog+X_t%2B1%5D%7D&bg=ffffff&fg=000000&s=0&c=20201002) .

.

![\displaystyle {\mathbb P}(\bar X_t\ge K)\le\inf_{x < K}\frac{{\mathbb E}[(X_t-x)_+]}{K-x}.](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%7B%5Cmathbb+P%7D%28%5Cbar+X_t%5Cge+K%29%5Cle%5Cinf_%7Bx+%3C+K%7D%5Cfrac%7B%7B%5Cmathbb+E%7D%5B%28X_t-x%29_%2B%5D%7D%7BK-x%7D.+&bg=ffffff&fg=000000&s=0&c=20201002)

, there exists a martingale with this terminal distribution for which (

, there exists a martingale with this terminal distribution for which ( in (

in (![\displaystyle {\mathbb E}[F(\bar X_t)]\le{\mathbb E}[G(X_t)]](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle++%7B%5Cmathbb+E%7D%5BF%28%5Cbar+X_t%29%5D%5Cle%7B%5Cmathbb+E%7D%5BG%28X_t%29%5D+&bg=ffffff&fg=000000&s=0&c=20201002)

. The aim of this post is to show how they have a more general `pathwise’ form,

. The aim of this post is to show how they have a more general `pathwise’ form,

. It is relatively straightforward to show that (

. It is relatively straightforward to show that ( will be of the form

will be of the form  for an increasing right-continuous function

for an increasing right-continuous function  , so

, so

, so can be used as the definition of

, so can be used as the definition of  . In the case where X is a semimartingale, integration by parts ensures that this agrees with the stochastic integral

. In the case where X is a semimartingale, integration by parts ensures that this agrees with the stochastic integral  . Since we now have an interpretation of (

. Since we now have an interpretation of ( to be a cadlag real-valued function. Hence, we reduce the martingale inequalities to straightforward results of real-analysis not requiring any probability theory and, consequently, are much more general. I state the precise pathwise generalizations of Doob’s inequalities now, leaving the proof until later in the post. As the first of inequality of theorem

to be a cadlag real-valued function. Hence, we reduce the martingale inequalities to straightforward results of real-analysis not requiring any probability theory and, consequently, are much more general. I state the precise pathwise generalizations of Doob’s inequalities now, leaving the proof until later in the post. As the first of inequality of theorem  ,

,

.

. then,

then,

.

.

.

.